Higher inflation or slower growth? The tug-of-war facing markets

Key takeaways:

- Markets are weighing whether the current energy price spike proves temporary—or begins to meaningfully erode underlying demand.

- Q1 earnings season may help clarify that trade-off, as investors look to management teams for guidance on demand, pricing power, and resilience if energy-related pressures persist.

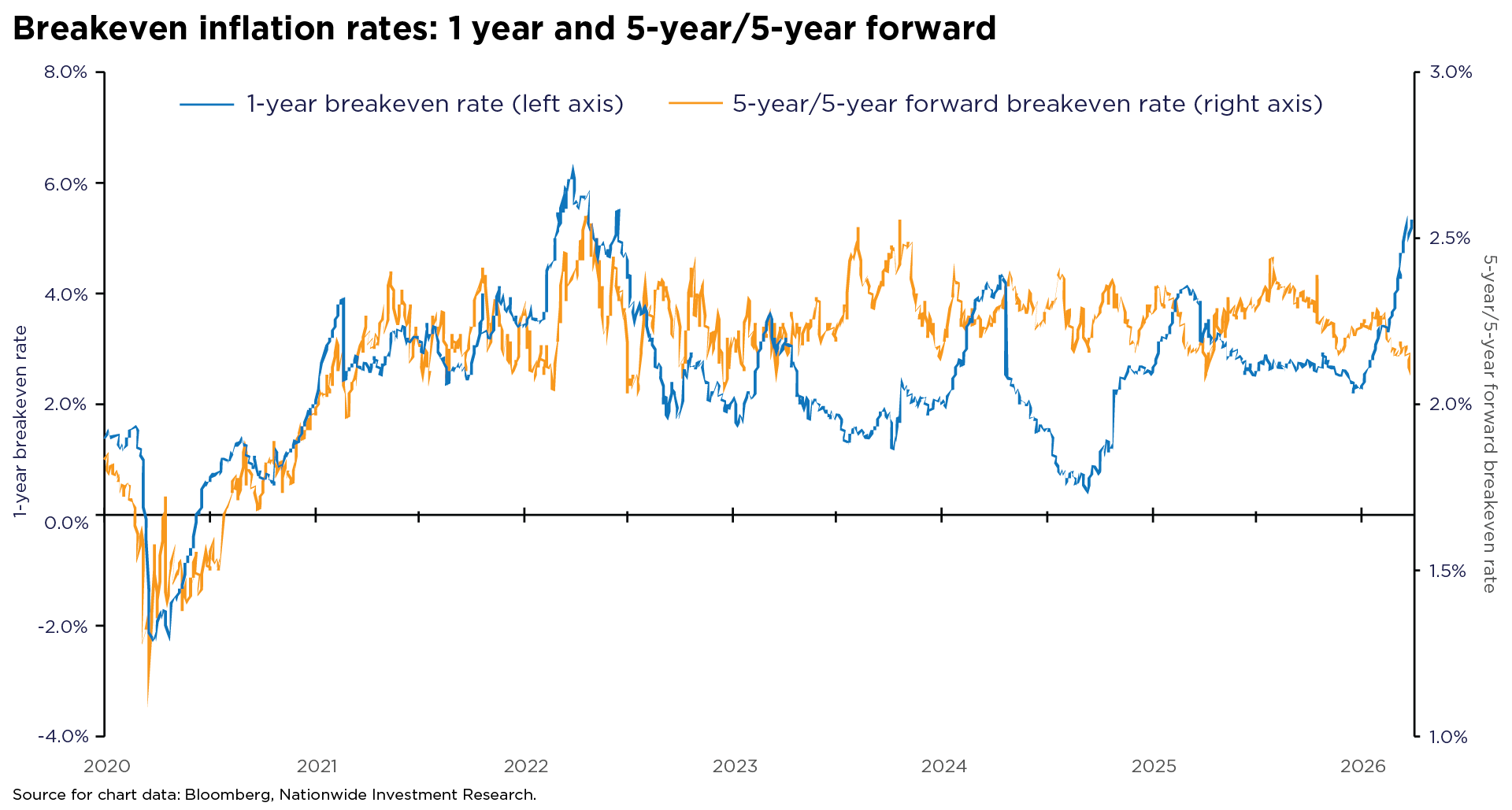

04/08/2026 – One of the clearest signals from the latest geopolitical shock is that markets remain torn over which risk matters more: the near-term inflation impulse from higher energy prices or the more durable drag on growth that often follows a disruptive supply shock. This push and pull is visible in breakevens, with the one-year inflation rate moving higher even as the 5-year/5-year forward breakeven has drifted lower.

The one-year breakeven inflation rate reflects market expectations for inflation over the next year. By contrast, the 5-year/5-year forward rate captures inflation expectations for the five-year period beginning five years from now. As the chart shows, near-term inflation expectations surged in March, pointing to inflationary spillovers from oil, natural gas, aluminum, and a range of downstream industrial inputs. This is precisely the kind of commodity-driven inflation that dominated headlines and revived the well-worn “stagflation” narrative.

History matters here. Commodity-driven price spikes often prove self-correcting because they are, by nature, demand-destructive. When the shock is rooted in physical supply constraints, the initial impact is a rise in headline inflation—but over time, higher prices tend to erode the very demand needed to keep those increases in place.

While the longer-term economic fallout from the conflict remains difficult to assess, the recent decline in the 5-year/5-year forward breakeven rate appears to reflect a confluence of factors rather than a single, clear signal. Part of the move likely stems from shifting expectations around demand, growth, or even the prospect of de-escalation once the initial shock fades—but these readings should be interpreted with caution.

Just as importantly, the decline also appears influenced by real-rate dynamics, with longer-dated real yields rising faster than their shorter-dated counterparts, alongside broader liquidity and positioning effects in the TIPS market. In other words, several crosscurrents are pushing the 5-year/5-year breakeven lower. This move is best viewed as a composite signal—reflecting growth uncertainty, inflation repricing, and tighter financial conditions—rather than a clean read on any single factor.

Q1 earnings reports may prove pivotal in restoring some line of sight. As earnings season unfolds, the emphasis will likely shift away from backward-looking results and toward forward guidance, with investors looking to management teams for clarity on demand durability, labor needs, pricing power, and how much flexibility they retain if energy-related pressures persist.

At this stage, markets are effectively weighing whether today’s commodity-driven price spike proves transitory or begins to materially erode underlying demand. Corporate guidance won’t resolve that tension outright, but it should provide investors with a clearer sense of how management teams are assessing the balance of risks.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.