How much is the "wealth effect"

propping up economic growth?

Key takeaways:

- The two major sources of household wealth—financial assets and real estate—have provided powerful tailwinds supporting consumer spending and economic growth.

- A market downturn could pose the greatest risk to the resilience of consumer spending and the sustainability of the economic expansion.

02/12/2025 – With fourth-quarter GDP showing consumer spending increasing by 4.2%, the largest quarterly upturn since early 2023, and the current earnings season commentary corroborating the resilience of the consumer, the consistent underestimation of economic growth during the past few years might be largely because of the “wealth effect.”

Essentially, the wealth effect suggests that consumers spend more when their wealth increases. The two major sources of household wealth—financial assets and real estate—are both hovering at or around all-time highs. The latest Federal Reserve data reveals that household net worth reached nearly $169 trillion in the third quarter of 2024, fueled by strong growth in housing (2020-22) and the back-to-back calendar-year gains of over 20% for the S&P 500® Index (2023-24). These are the powerful tailwinds supporting the wealth effect.

The wealth effect can be a powerful stimulant for economic growth. For instance, according to Ned Davis Research, each 1% increase in household net worth is associated with a 0.4% year-over-year increase in consumption in the following quarter. That said, a deep and prolonged equity market correction would not bode well for consumption, as shoppers would likely curtail discretionary purchases and households would shift to saving more and spending less. High-income consumers, in particular, have significantly contributed to overall U.S. household consumption, driven by a robust wealth effect over the past five years.

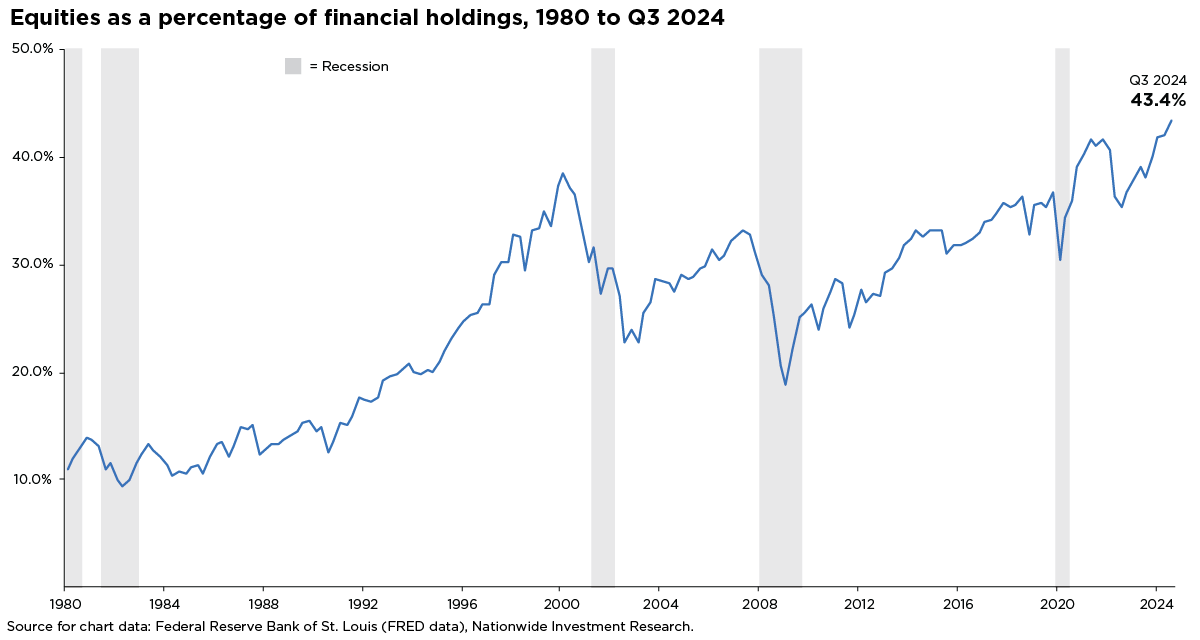

Given the strong spending behavior driven by the powerful wealth effect over the past several years, investors should know household equity allocations are at all-time highs (see the accompanying chart). As 2025 unfolds, a market downturn could pose the greatest risk to high-income households in their willingness and ability to spend. That might undermine the health of the U.S. consumer and blunt the economy’s current momentum.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.