Money market funds see strong flows—

but beware the undertow

Key takeaways:

- The combination of strong equity returns and higher yields in cash and fixed income reflects a more balanced opportunity set—one that blends long-term discipline with flexibility across developing market conditions.

- Recent fund flows and trading data point to a structural shift, with investors using volatility as an opportunity to manage risk and broaden diversification across risk assets.

05/20/2026 – Since 2022, financial assets across the risk spectrum have undergone a significant repricing as Federal Reserve rate hikes not only slowed demand but also reintroduced competition for capital. For the first time in years, investors could earn meaningful income from cash and bonds while still taking part in equity market growth.

Equities have proven more resilient than many expected, with a new bull market emerging nearly in parallel with the Fed’s rate-hiking campaign. The result is a more balanced opportunity set, where capital is no longer pushed out along the risk curve by necessity but allocated by choice. This hasn’t been a wholesale retreat from risk, but a more nuanced redistribution of capital across liquidity, income, and growth-oriented assets.

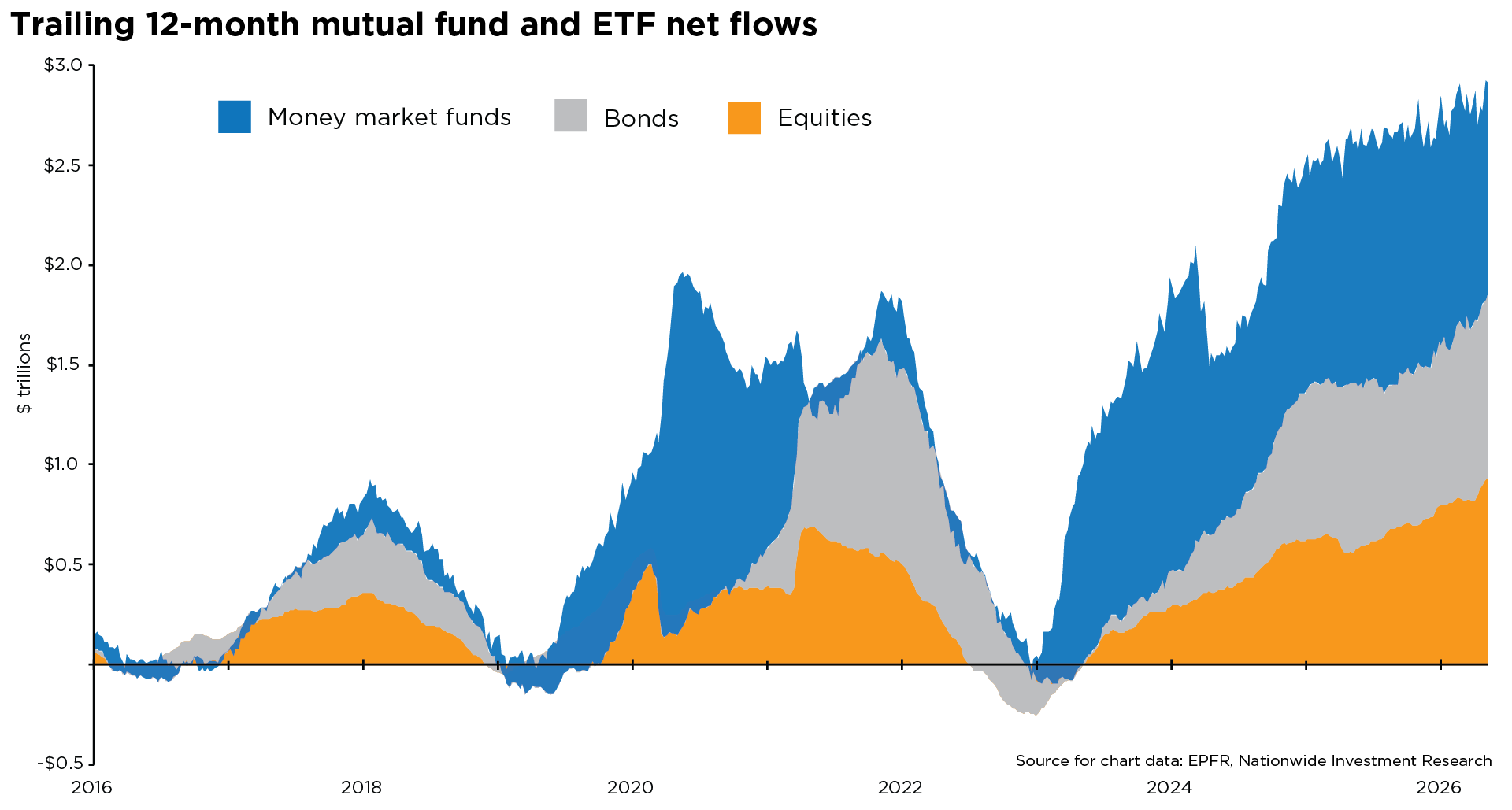

We can see this shift clearly in money market fund inflows. Balances are approaching $8 trillion—up over 70% since the onset of the 2022 hiking cycle. Higher short-term rates have transformed cash from a dormant allocation into a legitimate source of yield and, importantly, optionality.

Rather than signaling defensiveness, elevated cash levels may reflect a rational response to an environment where liquidity once again competes for capital on more equal footing with risk assets. That said, with inflation’s recent persistence, the risk of negative real returns remains a quiet but meaningful headwind to long-term wealth creation.

Fixed income has undergone a similar transformation, with higher rates initially pressuring prices but ultimately restoring the asset class’s income appeal after years of scarcity. That re-engagement has increasingly taken place through ETFs—particularly active strategies designed to manage duration and credit risk more precisely.

Active fixed income ETFs have captured roughly 45% of year-to-date flows, compared to about 10% in 2022, according to Strategas. Those flows may offer a clearer signal of investor preferences: the concentration in ultra-short and short-duration exposures suggests a focus on flexibility and control rather than a simple reach for yield.

Equities have remained notably resilient despite a steady cadence of market shocks. Retail investors, in particular, have continued to lean into periods of volatility by adding exposure, reinforcing the buy-the-dip dynamic that has defined much of the post-COVID cycle. Trading volumes for index-linked ETFs have historically risen during episodes of market stress—and again during the subsequent rebound—according to Goldman Sachs data. This behavior extends beyond broad selloffs: retail activity also tends to concentrate in individual equities following sharp drawdowns, often supplemented by margin and leveraged ETF exposure.

Additionally, Goldman Sachs notes that this impulse is likely no longer episodic but structural, with retail investors now accounting for roughly 20% of U.S. stock market trading volume—a meaningful step up from prior cycles—and holding around $12 trillion in equity assets in self-directed brokerage accounts. The continued expansion of the ETF ecosystem has likely amplified this dynamic by lowering trading friction and enabling more precise allocations across asset classes, factors, and sectors.

Taken together, recent flows and trading patterns point to a structural shift toward more tactical, liquidity-driven engagement, where investors increasingly use volatility as an opportunity to manage risk and broaden diversification across risk assets.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.