Q2 earnings: Resilience over fear in a volatile market

Key takeaways:

- S&P 500® Index earnings and revenues are surpassing expectations at a pace not seen in years.

- Surprising results suggest companies are strategically adapting to external shocks, including tariff-related disruptions.

08/20/2025 – Second-quarter earnings season kicked off amid a haze of uncertainty—persistent market volatility, mixed policy signals, and a rapidly evolving global economic backdrop. Companies navigated a range of challenges, from the short-lived pause on “Liberation Day” tariffs to softening consumer sentiment. As a result, analysts trimmed their Q2 earnings forecasts significantly, dropping from 9.2% in March to just 3.8% by the end of June.

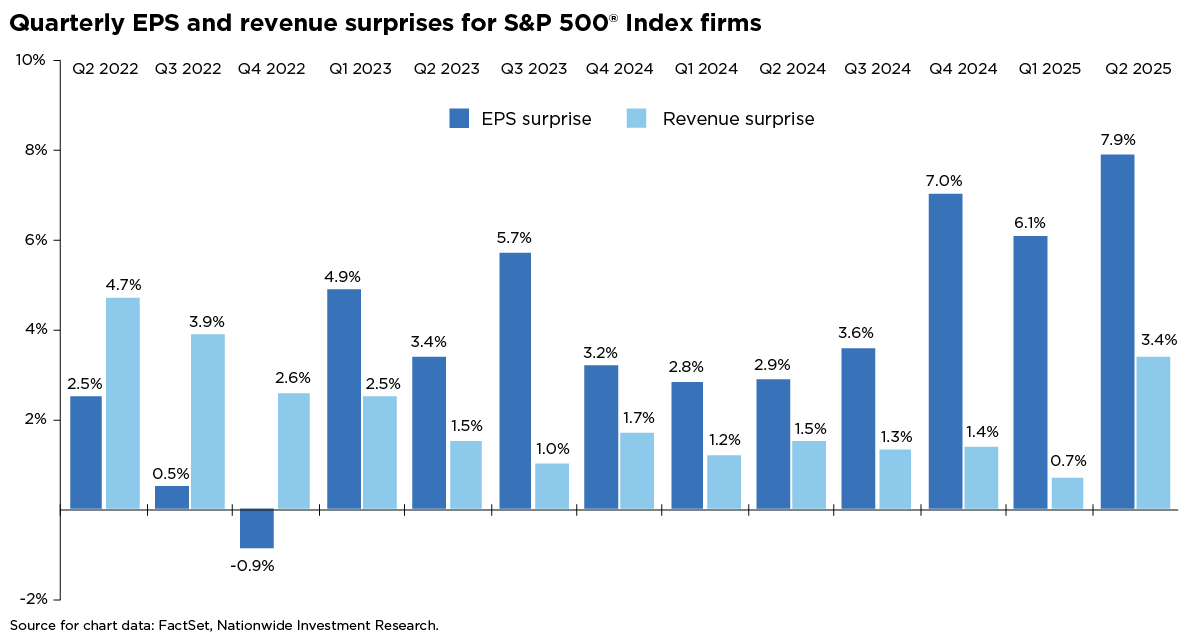

The downward revision sparked valid concerns among investors about the staying power of the equity bull market. But once Q2 results started rolling in, earnings season delivered a clear upside surprise—showcasing the resilience of corporate America. With 91% of companies reporting, 82% of S&P 500® Index firms beat bottom-line expectations, posting an average earnings surprise of 8.4%. Both metrics came in well above their five- and ten-year historical averages.

Earnings momentum picked up significantly as the quarter progressed, with S&P 500 EPS growth now tracking above 11% year-over-year—more than double what analysts expected in early July. This sharp upward revision hints that early concerns over trade-related disruptions may have been exaggerated.

One of the more telling signals from Q2 may lie in top-line performance. About 80% of companies beat second-quarter revenue expectations—a pace that, if maintained, would mark the highest revenue beat rate since Q2 2021. The average revenue surprise of 2.3% also topped historical norms, representing the strongest top-line outperformance since Q1 2023.

While part of the outperformance can be chalked up to a lower bar—thanks to aggressive downward revisions ahead of earnings season—the broad and consistent revenue beats suggest a more resilient economic backdrop. Full-year earnings estimates for 2025 and 2026 are not only stabilizing but trending higher. The momentum in revenue revisions stands out, with positive sales upgrades far outpacing EPS upgrades, likely supported by a weaker U.S. dollar.

Additionally, 86% of companies have reported positive three-month shifts in forward revenue—providing a strong rebuttal to earlier worries about pricing power and demand elasticity.

These developments show that companies aren’t just reacting to external shocks—they’re adapting with intention. Tactical moves like renegotiating with vendors, reworking supply chains, tightening general expenses, and flexing pricing strategies are coming together to build a more resilient corporate framework. It’s a theme that came up often in Q2 earnings calls.

Looking ahead, the staying power of top-line momentum will hinge on how tariff dynamics play out—and how consumers react to changing price signals. Even if markets hit a few bumps in the weeks ahead, any pullbacks may occur within the broader backdrop of a bull market that still appears fundamentally sound.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.