Soft dollar, hard data:

Rethinking the U.S. dollar weakness narrative

Key takeaways:

- Foreign investors are still buying U.S. assets—despite the dollar narrative.

- Dollar softness points to global expansion, not U.S. slowdown.

02/04/2026 – A mix of macroeconomic crosscurrents—shifting Fed signals, expanded fiscal spending, geopolitical tensions, and the prospect of yen intervention—has pushed the U.S. dollar lower over the past year. Those pullbacks have revived what many in the market refer to as the “dollar debasement trade.”

Dollar debasement reflects a view that the dollar’s purchasing power will erode over time. Investors position for this by leaning into traditional stores of value—gold, inflation-resilient real assets, and selective non-dollar exposures—when policy, fiscal, or global rate dynamics suggest the currency’s real value may weaken.

Last year’s surge in precious metals—gold up 65% and silver nearly 175%—offers a clear illustration of the dollar-debasement theme at work. These outsized moves have also sparked speculation that investors may rotate out of U.S.-denominated assets in search of protection against further dollar weakness.

Yet beneath the market buzz that often builds around volatility and momentum, the data tell a different story: foreign investors continue to buy U.S. assets at a strong pace, challenging the debasement narrative that has dominated recent market commentary.

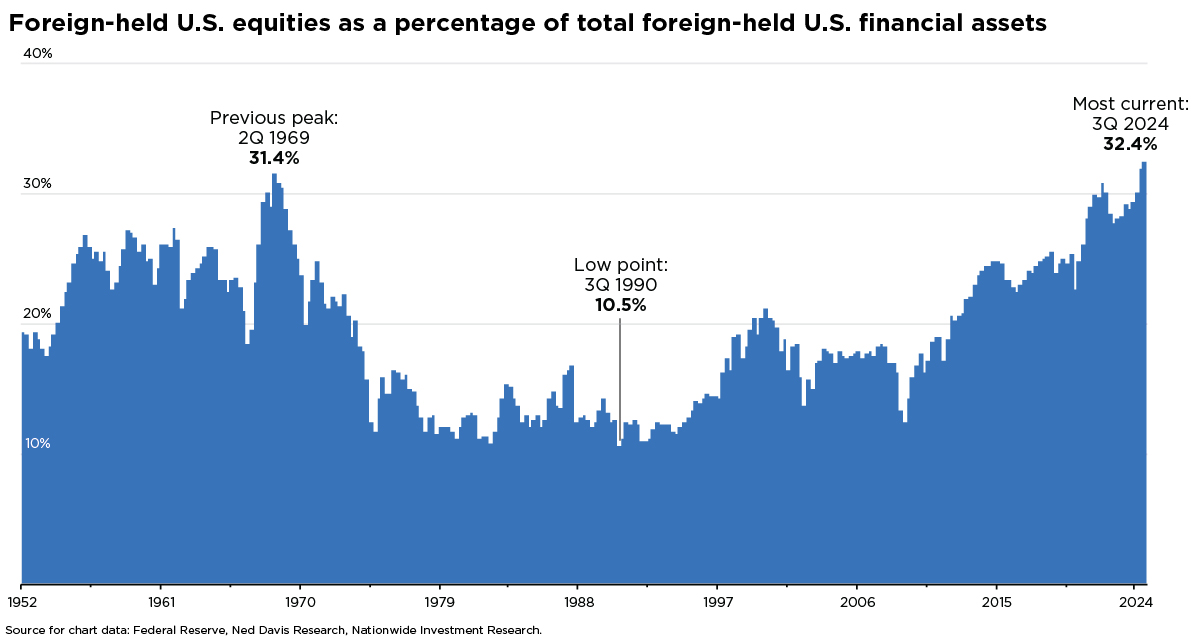

When markets are awash in competing opinions, flow-of-funds data can help clarify where real conviction sits. Foreign ownership of U.S. securities climbed to nearly $35 trillion in Q3 2025—an all-time high. And despite all the chatter about international markets outperforming the U.S. in 2025, foreign investors have continued to lean into U.S. equities. Foreign equity holdings climbed to $20.8 trillion last year—another record—representing 32% of all foreign-held U.S. financial assets and surpassing the previous high set during the 1968 bull-market peak. Goldman Sachs adds further context: from January through November 2025, foreign investors bought $628 billion in U.S. equities.

While dollar softness may persist into 2026, it appears to signal less about U.S. economic vulnerability—especially given the continued strength in corporate profits—and more about a broadening global expansion. A healthier global backdrop can improve earnings translation, enhance the competitiveness of U.S. firms abroad, and boost international returns for dollar-based investors.

Today’s dollar weakness looks less like a verdict on U.S. fundamentals and more like a byproduct of broader global diversification. It’s a reminder of the value—for clients and portfolios—of maintaining a well-diversified asset mix.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.