Stocks and bonds are moving together—now what for portfolios?

Key takeaways:

- As stock-bond correlations turn positive, advisors are fielding more client questions about how effective traditional diversification remains in the current environment.

- With stocks and bonds increasingly influenced by the same macro forces, diversification requires a more deliberate approach—placing greater focus on how portfolios are constructed while remaining grounded in core risk principles.

06/10/2026 – Stocks and bonds have been moving in tandem for much of the past several months. As stock-bond correlations rise, advisors are fielding more questions about whether traditional diversification strategies can still deliver as intended.

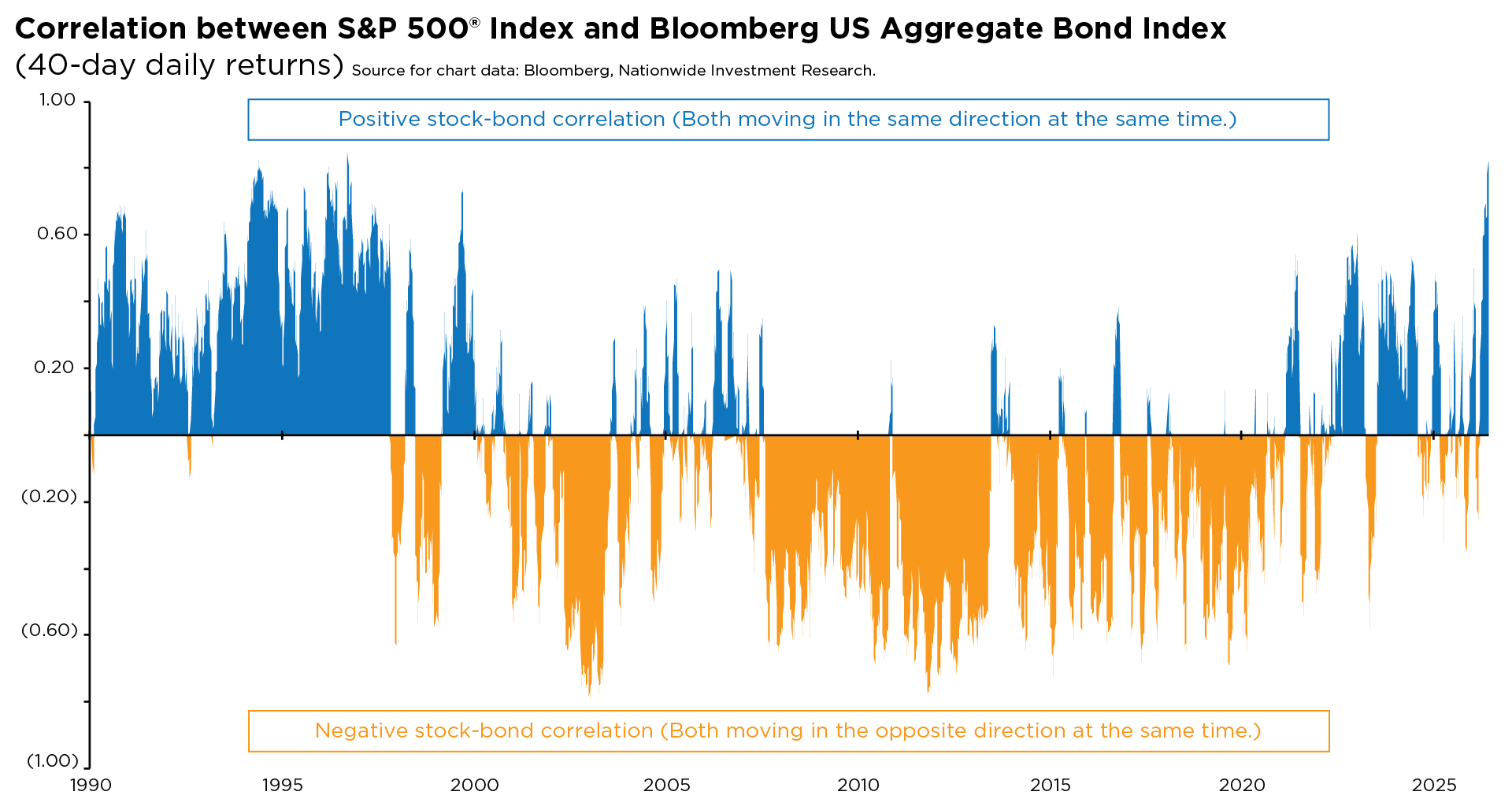

For much of the past two decades, the answer was largely yes. Stocks and bonds typically moved in opposite directions (i.e., negative correlation), with fixed income providing a reliable hedge during equity drawdowns. More recently, that relationship has been less dependable, as stocks and bonds have increasingly moved in sync—challenging the benefits of passive diversification.

Short-term correlations—measured by the rolling 40-day relationship between the S&P 500® Index and the Bloomberg U.S. Aggregate Bond Index—have climbed to their most positive levels since 1999 (see chart). This points to a market backdrop where uncertainty around policy (fiscal and monetary), inflation, growth, and geopolitics is influencing asset classes in a more unified way.

Inflation uncertainty appears to be the dominant driver in the current market environment, reflected in rising real interest rates. Higher rates signal not only persistent price pressures, but also a more constructive long-term growth outlook—partly tied to expectations for AI-driven productivity gains. The result: both equities and bonds are increasingly exposed to the same set of macro forces.

This dynamic underscores how dependent cross-asset relationships are on the prevailing macro environment. When inflation is low and stable, growth concerns tend to dominate—supporting negative correlations, as bonds often rally when equities weaken. In more inflationary settings, however, elevated price pressures can constrain the Federal Reserve’s ability to cut rates, creating a backdrop where both stocks and bonds may come under pressure at the same time. Diversification hasn’t broken down, but it has become more dependent on the underlying economic data.

The traditional 60/40 framework remains a durable foundation—especially as higher nominal and real yields have improved the outlook for fixed income. That said, advisors may need to adapt how they implement it. This could include broadening diversification across assets with different macro sensitivities and being more deliberate within equities, where concentration risk has increased meaningfully.

Staying anchored to strategic allocations, maintaining broad and intentional diversification, and rebalancing with discipline can help portfolios navigate uncertainty. Periods of volatility and shifting asset relationships aren’t aberrations—they’re a natural feature of evolving market conditions. While the environment may change, the core principles remain intact.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.