Understanding concentration risk

in the stock market

Key takeaways:

- As concentration risk has increased, financial professionals may want to revisit portfolio allocations in year-end client meetings.

- In 2026, midterm elections and stimulative tax measures may help boost defensive and consumer-oriented sectors.

12/03/2025 – Concentration risk in the S&P 500® Index is drawing attention in today’s tech-driven bull market. The ten largest companies—just 2% of the Index—now account for about 41% of its total market cap. That’s well above the peak of the dot-com era in 2000, when the top ten represented roughly 27%.

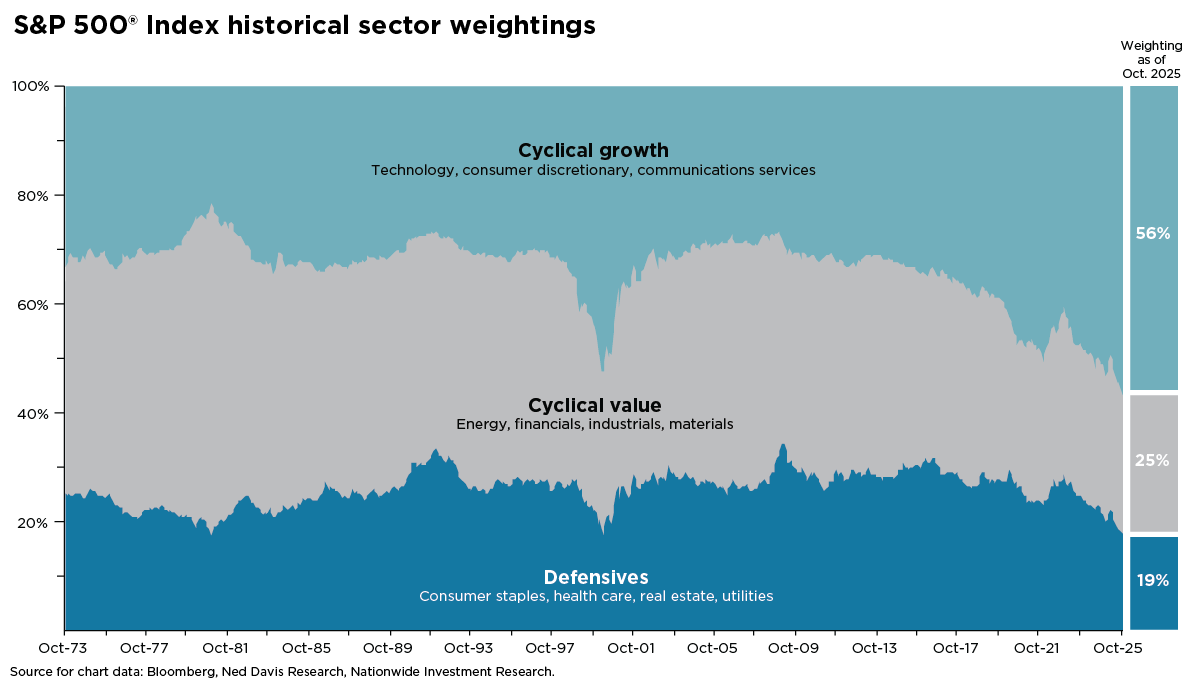

The Magnificent 7—Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia and Tesla—have driven much of the market’s gains. In fact, they accounted for 56%, 63% and 55% of the S&P 500’s annual price returns in 2022, 2023 and 2024, respectively. Their surge has reshaped the Index, pushing traditional value sectors like energy, materials, industrials and financials to the sidelines, while growth-oriented areas such as technology, consumer discretionary and communication services take center stage.

Defensive sectors—consumer staples, health care, utilities and real estate—have also lost ground. Their combined weight in the S&P 500 has dropped from a historical average of 36% to just 20%. Meanwhile, the remaining sectors now account for 80% of the Index, well above their long-term average of 64% since 1995. (See the accompanying chart.)

As you plan for client meetings in the year ahead, it may be worth revisiting tactical portfolio positioning—especially given the concentration risk in today’s market. Another factor to watch: midterm elections. Historically, the second year of a presidential term leading up to midterms has been the most volatile of the four-year cycle. The S&P 500 has averaged an intra-year decline of 19% during these periods, compared with average gains of 12% in the other three years.

One potential bright spot: midterm-year volatility often favors defensive sectors like health care and consumer staples. Looking ahead to 2026, tax changes could inject about $150 billion into household budgets—boosting disposable income and potentially lifting stocks in consumer discretionary and staples sectors.

Sector weights outside of technology, consumer discretionary and communication services are likely to remain limited into 2026. Advisors may want to rebalance portfolios by reducing overweight positions in these areas, maintaining proper diversification, and considering a tactical tilt toward defensive sectors to help buffer against potential volatility. These steps can help reduce downside risk if high expectations for growth stocks meet a more cautious market backdrop in the year ahead.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.