What will surprise markets in 2026?

Early signals to watch

Key takeaways:

- Markets are pricing in strong tailwinds for 2026—so expectations matter more than ever.

- Economic surprises will drive the narrative—and advisor framing will be key.

01/28/2026 – Judging by where equities are trading today, investors appear to be pricing in meaningful tailwinds for growth as we head into 2026. Markets are anticipating roughly 175 basis points of Fed rate cuts, alongside potential fiscal stimulus, lighter regulatory burdens, and a range of tax incentives—all aimed at supporting corporate profitability and consumer spending.

These tailwinds aren’t likely to unfold in a straight line. In the months ahead, markets will parse each data release through the lens of expectations versus actual outcomes. Stronger-than-expected economic activity, consumer spending, or corporate earnings would help validate the bullish backdrop and support risk assets. But disappointments—especially around profits or consumer health—could easily slow that momentum.

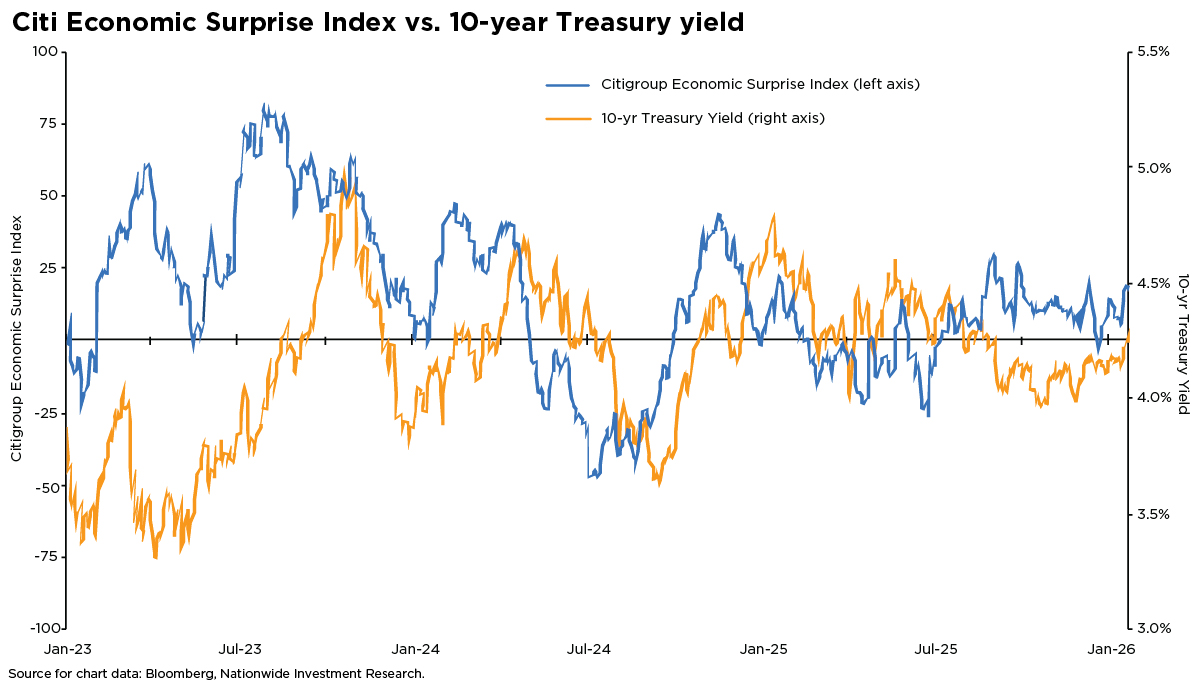

This is where the Citi Economic Surprise Index becomes a useful gauge for tracking incoming data and its potential implications for earnings expectations. When economic releases come in above forecast, the Index moves higher—signaling that the economy is outperforming expectations. That often pushes Treasury yields up as markets price in stronger and more durable growth. Conversely, weaker-than-expected data typically pulls the Index lower and tends to compress yields as growth prospects soften.

The accompanying chart illustrates how this pattern has unfolded in recent years—and why it’s likely to remain a key market driver in 2026. Any downside surprises in growth would also raise concerns about the durability of corporate margins and the strength of current earnings expectations, which—as of this writing—call for roughly 15% earnings growth for the S&P 500® Index over the next year.

The emerging rotation in market leadership—including the recent stretch of small-cap outperformance relative to the S&P 500—highlights investors’ preference for areas tied to accelerating economic growth and positive earnings revisions. This shift essentially reflects a bet on improving fundamentals and a broader sense of economic optimism. Any data that challenges those assumptions could introduce additional volatility and lead to choppier market action.

For advisors, the Citi Economic Surprise Index can help frame the current market climate, but it shouldn’t drive investment decisions. A steadier approach is to keep the focus on fundamentals—building and maintaining a well-diversified portfolio that aligns with each client’s risk tolerance, time horizon, and long-term objectives.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.