Help clients manage Social Security worries with annuities

Key takeaways:

- Confidence in Social Security is declining. Many Americans rely on the program for retirement income but worry about potential benefit reductions or funding shortfalls.

- Financial professionals can turn this concern into planning opportunities. Diversifying retirement income may help clients feel greater confidence in their long-term financial security.

- Guaranteed income products—including annuities—can complement Social Security and help clients gain a sense of confidence should monthly benefits decrease in the not-too-distant future

03/27/2026 — For decades, Americans have viewed Social Security as the foundation of their retirement income. But confidence in the program’s future has been slipping. For financial professionals, that creates both a challenge and an opportunity. Clients still expect Social Security to play a major role in retirement, yet many aren’t convinced it will deliver the benefits they anticipate.

That growing uncertainty has prompted more consumers to look for additional sources of guaranteed income. In that environment, annuities can help strengthen retirement income strategies while addressing clients’ concerns about potential changes to Social Security.

Growing concerns about Social Security and retirement income security

Americans’ concerns about Social Security are widespread. In fact, Social Security is a top five overall worry for Americans. More than half (52%) worry a great deal about the Social Security system, while another 24% worry a fair amount.1

Their main concern? Three out of four Americans fear the Social Security program could run out of funding during their lifetime, according to the Nationwide Retirement Institute 2025 Social Security survey.2 In the same research, eight out of 10 workers and seven out of 10 retirees say they’re at least somewhat concerned about significant changes to the U.S. retirement system.

These worries are deepening. Faith in Social Security has trended downward for years. A 2025 AARP survey on Social Security opinions and attitudes found confidence in the program dropped from 43% in 2020 to 36% in 2025—the lowest level recorded in 15 years.

Taken together, these findings highlight a growing confidence gap in retirement income planning. Social Security remains a central pillar of retirement income, but many Americans aren’t sure it will deliver the level of benefits promised.

Dependence without confidence

Despite these concerns, Social Security still plays a major role in retirement income planning. The large majority (87%) of workers expect Social Security to be one of their top sources of retirement income, and 94% of retirees report that it already is.3

This creates an interesting dynamic for financial professionals. Clients expect Social Security to be a key part of their retirement income strategy. Yet many don’t fully trust the program’s long-term stability.

That tension often surfaces in planning conversations. Clients may ask whether benefits will be reduced, whether the retirement age will increase, or how other future policy changes could affect the amount they ultimately receive.

Turning uncertainty into a planning opportunity

Financial professionals can’t predict the future of Social Security policy. But they can help clients build retirement income strategies that rely less on any single source of income.

One way to do that is by incorporating additional sources of guaranteed income. These solutions can help stabilize a retirement plan by providing predictable cash flow that isn’t tied to future policy decisions.

In many cases, annuities can help provide that added layer of certainty. Because annuities offer contractually guaranteed income, they can serve as a reliable complement to Social Security benefits.

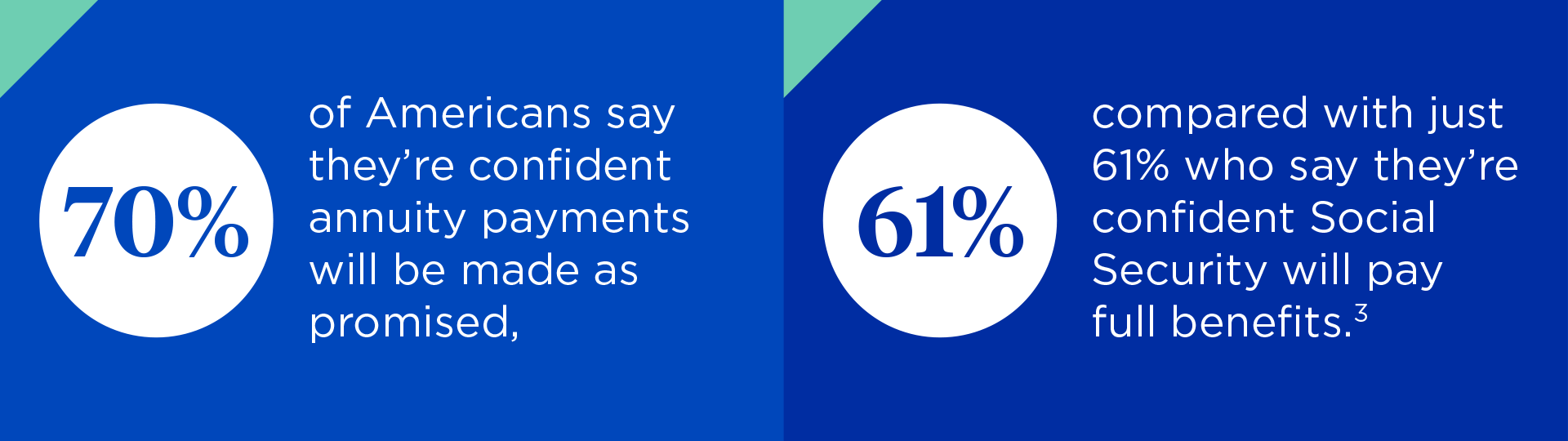

Research suggests many consumers already view annuities this way. Seventy percent of Americans say they’re confident annuity payments will be made as promised, compared with just 61% who say they’re confident Social Security will pay full benefits.3

Building a diversified retirement income strategy with guaranteed income

Concerns about Social Security aren’t likely to disappear anytime soon. But those concerns can open the door to more productive planning conversations. By helping clients combine Social Security with other sources of guaranteed income, financial professionals can reduce reliance on any single program while improving overall income stability.

Annuities can play an important role in that process. When integrated thoughtfully into a broader retirement strategy, they can help address the confidence gap many Americans feel about their future income.

Ultimately, financial professionals play a key role in helping clients prepare for retirement with greater certainty. As questions about Social Security continue, building diversified and dependable income streams may be one of the most effective ways to help clients protect their retirement checks.

Author

Brad Carrier

Vice President, Brokerage Annuity Distribution

Brad Carrier is Vice President of Brokerage Annuity Distribution at Nationwide Financial. In this role, Brad is responsible for the commission-based annuities business across all channels, including broker/dealers, wires, and banks.

Trending articles

Long-term care is a topic many people don’t talk about, but the need for planning is real. View our latest insights from our LTC survey that detail how consumers are feeling.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.