The new annuity conversation: Meeting rising client demand with better guidance

Key takeaways:

- More clients are asking about annuities and turning to their financial professional for guidance as interest in guaranteed lifetime income continues to grow.

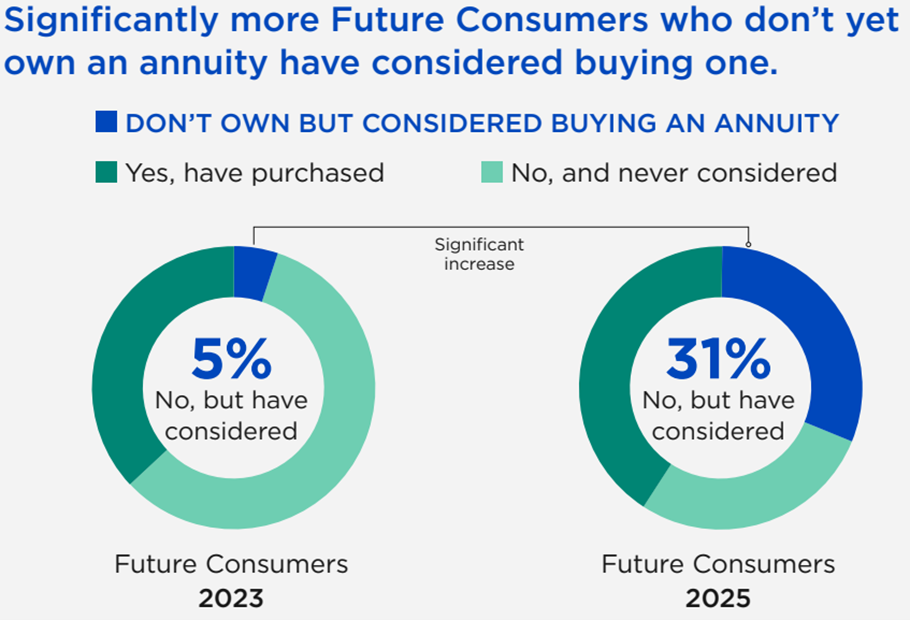

- Among future consumers who don’t yet own an annuity, consideration rose from 5% in 2023 to 31% in 2025—a more than six-fold increase.1

- Annuity owners are significantly more confident about retiring on time than non-owners—76% vs. 49%—underscoring the role guaranteed income can play in retirement outcomes.2

- Financial professionals who engage proactively in annuity conversations are better positioned to meet evolving client expectations and help support stronger retirement outcomes.

05/27/2026 — More clients are asking about annuities and looking to their financial professional for guidance on how guaranteed lifetime income fits into their retirement plan.

Why the growing interest? Many people are concerned about turning their savings into income that will last, especially as they get closer to retirement and start thinking more seriously about how they'll cover expenses once they’re no longer collecting a paycheck.

Nationwide’s Future Annuity Consumer research reflects that shift. Among future consumers who don’t yet own an annuity, 31% have considered buying one, up from just 5% in 2023. That’s a more than six-fold increase in two years.1

At the same time, annuity owners report significantly higher levels of confidence about retirement. Nationwide’s 2025 Retiree Insights research found that 76% say they’re confident they’ll retire on time, compared to 49% of non-owners.

June is Annuity Awareness Month, making it a good time to revisit how annuities fit into the retirement planning conversations you're having with clients. If you already use them, now may be a good time to reassess how they fit into your broader retirement income planning approach. For financial professionals who don't use annuities—or don't use them as often—now may be a good time to take another look.

Clients are actively seeking annuity guidance

Many clients are looking for help understanding how to create sustainable retirement income and reduce the risk of outliving their savings. Those are exactly the challenges guaranteed lifetime income annuities are designed to address.

Nationwide’s Future Annuity Consumer Research found:

- 63% of future consumers now go to their financial professional first when researching annuities, up from 49% in 2023 (a 29% increase).1

- 78% have discussed annuities with their financial professional, up from 66%.1

Consider initiating annuity conversations before clients ask. If they don't get information from you, they'll look elsewhere, whether that's another financial professional or a direct-to-consumer platform.

Getting ahead of these conversations can help build trust because it shows clients you're thinking proactively about their long-term retirement security.

Why annuities help close the retirement confidence gap

Guaranteed lifetime income products can help address some of the biggest concerns clients have about retirement.

When a portion of their income is guaranteed regardless of market conditions, clients don't have to wait for the perfect moment to retire. The decision becomes less about timing the market and more about timing their life.

That confidence carries into retirement, too. Many people hesitate to spend, even when their plan supports it, worried that drawing down assets too quickly will leave them with a shortfall later. Annuities can help ease that hesitation. In the 2025 Retiree Insights research, six in 10 financial professionals said these products helped improve their clients' comfort with spending in retirement; a sentiment echoed by 37% of retirees who own an annuity.2

Clients who feel more secure about their income often feel more confident in the plan overall. That can lead to more productive planning conversations and fewer reactive decisions.

Guaranteed income is now a core client expectation

For many clients, guaranteed lifetime income has become an essential part of retirement planning conversations. It's the second most desired feature in a financial product, reflecting a meaningful shift in what clients are looking for when they think about retirement.

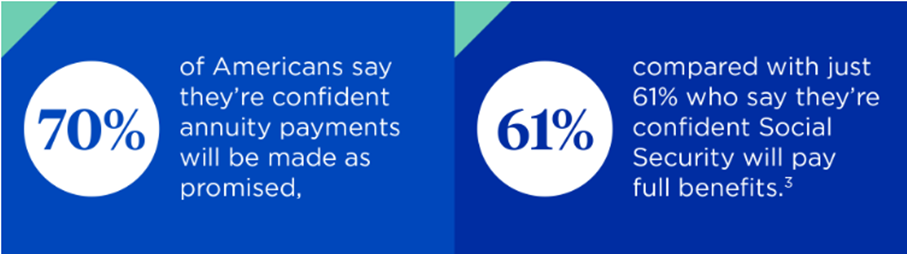

Concerns about the future of Social Security are part of what’s driving interest in guaranteed income solutions. 2025 Retiree Insights research shows that 70% of consumers are confident annuity payments will be made as promised, compared to just 61% who feel the same way about Social Security.3

That's especially meaningful for clients who don't have a pension to fall back on. For them, an annuity can help fill that gap by providing a reliable income stream alongside Social Security.

How to start annuity conversations with clients

Bringing annuities into the conversation doesn’t require a different planning process. In many cases, it’s about incorporating them more consistently into the one you already have. Here are some simple ways to do that:

Normalize the conversation

Start with existing discovery and review meetings. A few targeted questions can naturally surface whether a guaranteed lifetime income discussion makes sense, such as "How important is a predictable income stream in retirement to you?" or "How confident do you feel about retiring on time with your current plan?" The goal is to make annuities a standard part of retirement income planning.

Coordinate annuities with the broader plan

Annuities work best as one component of a comprehensive retirement income strategy. A blended approach that combines guaranteed lifetime income with investments designed for growth gives clients both predictability and upside potential. The bottom line: annuities are a tool, not the whole toolbox.

Educate with clarity

Many clients don't fully understand how annuities work. A straightforward explanation of what guaranteed lifetime income is, how it fits into a retirement income plan, and what trade-offs to consider—including liquidity, fees, and insurer strength—goes a long way toward helping clients make informed decisions. Keep in mind, the goal is education, not a sales pitch.

Making annuity awareness month count

Clients are thinking differently about retirement income than they were even a few years ago, and many are turning to their financial professional with questions about annuities.

At the same time, annuity owners continue to report higher levels of retirement confidence than non-owners. And guaranteed lifetime income is increasingly becoming a core part of the retirement conversation, not a niche consideration.

Annuity Awareness Month is a natural moment to act on those insights, whether that means initiating annuity conversations more consistently, revisiting how you explain them, or updating client education materials. In doing so, you can make a meaningful difference in your clients’ clarity and confidence about retirement.

The goal, as always, isn't to sell more products. It's to make sure every client has the guidance they need to retire well, and that they're getting it from you.

Author

Brad Carrier

Vice President, Brokerage Annuity Distribution

Brad Carrier is Vice President of Brokerage Annuity Distribution at Nationwide Financial. In this role, Brad is responsible for the commission-based annuities business across all channels, including broker/dealers, wires, and banks.

Trending articles

Long-term care is a topic many people don’t talk about, but the need for planning is real. View our latest insights from our LTC survey that detail how consumers are feeling.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.