Don’t forget diversification

amid the semiconductor surge

Key takeaways:

- Pro-business tailwinds—including fiscal stimulus, easing trade frictions, improving liquidity, and regulatory support—could help leadership broaden beyond semiconductors.

- The greater risk isn’t missing additional upside in semiconductors or the broader AI trade, but underestimating rotation into more cyclical and rate-sensitive areas of the market.

05/13/2026 – Q1 earnings season for the AI hyperscalers (e.g., Alphabet, Amazon, Meta, Microsoft) was impressively strong, surpassed only by the remarkable parabolas in stock market charts that these results produced.

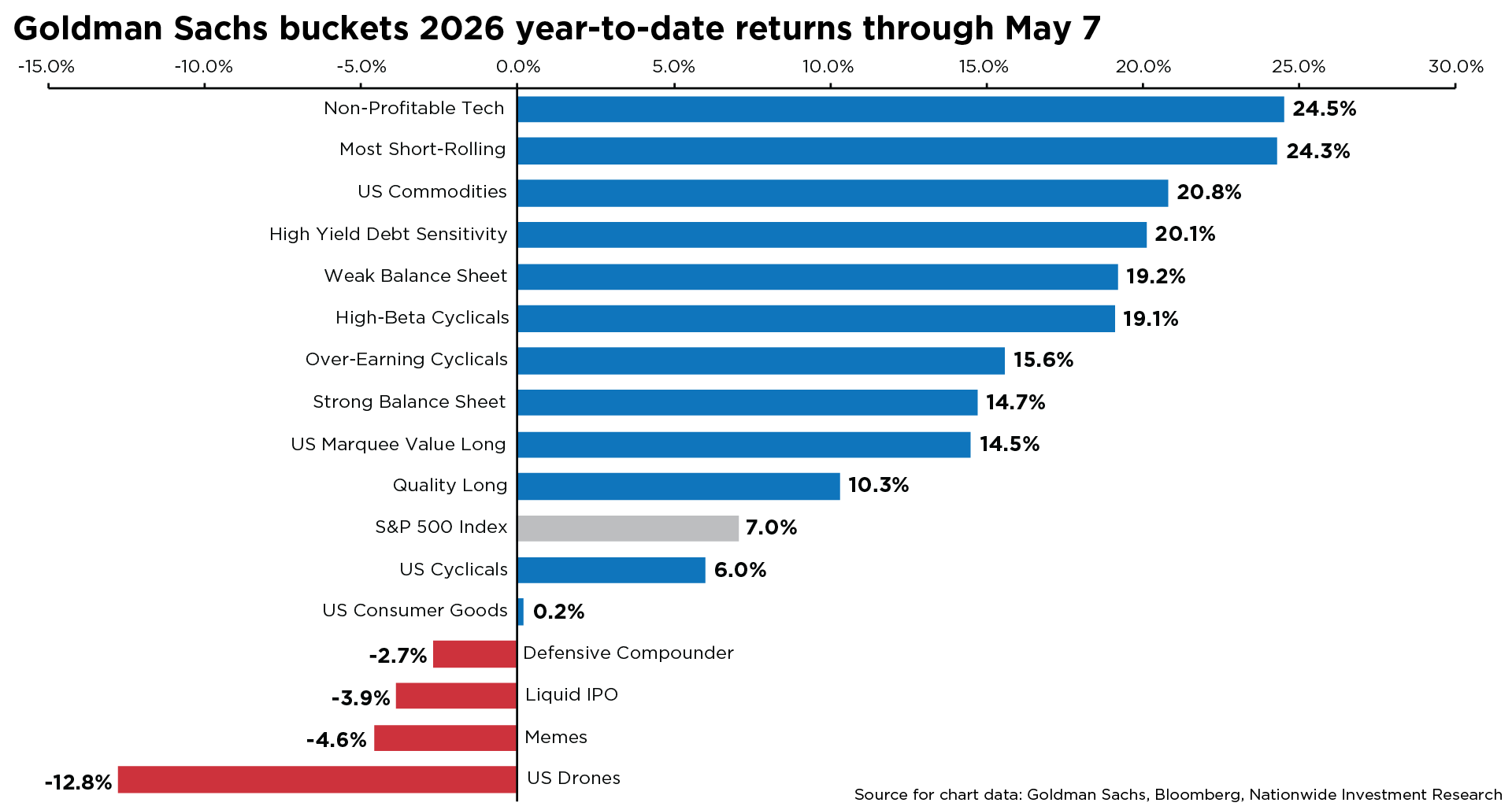

That reaction is hardly surprising given the unprecedented level of capital spending flowing through the AI ecosystem—investment that appears to be pulling future demand into today across the AI infrastructure stack. The surge has helped fuel roughly a 60% rally in the PHLX Semiconductor Sector Index since its March 30 low and has benefited long-duration growth proxies, including Goldman Sachs’s basket of non-profitable tech companies (see chart).

That said, part of the move also reflects a feedback loop, with investor sentiment increasingly drawn to the speed and scale of recent gains across AI-related trades. The enthusiasm has materially reshaped the equity landscape: semiconductors’ share of total market capitalization in the S&P 500® Index has jumped from roughly 6% in 2022 to nearly 17% today.

Investors may be witnessing one of the most powerful capex cycles in decades, but it’s important not to let that strength narrow the focus to a single corner of the market. The outlook for both market breadth—which has remained notably tight since the March 30 low—and the durability of earnings growth will ultimately depend on the broader macro backdrop, where a mix of cyclical tailwinds could support a more meaningful expansion in leadership beyond semiconductors alone.

It’s also important to recognize that the broader economic and policy backdrop remains supportive of wide-ranging business activity—even if recent market leadership hasn’t reflected it. A combination of fiscal stimulus, easing trade frictions, improving liquidity, and regulatory support continues to support economic growth and corporate earnings, laying the groundwork for a more diversified expansion in fundamentals.

Policies such as full expensing for capital investment and research and development are supporting corporate spending and cash flows, while tax-related tailwinds and resilient high-frequency data continue to signal strength in the real economy. For example, roughly $100 billion in capital gains tax relief and nearly $60 billion in consumer-related tax relief are expected to lift real incomes and discretionary spending.

At the same time, improving financial conditions and renewed credit growth should help extend market participation beyond the AI leaders. The building blocks for broader earnings growth and market breadth are in place—even if they don’t yet match the record-setting price action seen in semiconductors.

That said, some of these supports are likely to moderate in the coming months, placing greater emphasis on organic growth drivers. The more important question for investors isn’t whether the semiconductor cycle is nearing a peak, but whether portfolios are adequately diversified and positioned to participate in a broader expansion beyond a single dominant theme.

The greater risk isn’t missing additional upside in semiconductors or the broader AI trade, but underestimating the potential for rotation into more cyclical and rate-sensitive areas of the market. After parabolic gains in AI-linked assets, periods of extreme concentration and momentum often call for greater discipline—reinforcing the importance of diversification, rebalancing, and aligning portfolio risk with long-term objectives.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.