Geopolitics shakes markets,

but discipline shapes outcomes

Key takeaways:

- Geopolitical conflicts can move markets, but history shows that even sharp oil-driven shocks have been temporary.

- Investors who step out of the market during geopolitical stress often miss the strongest part of the recovery.

03/11/2026 – The outbreak of armed conflict in the Middle East has sent crude oil prices soaring and cast a shadow over the stock market during the first week of March. By the end of last week (March 6), West Texas Intermediate (WTI) climbed above $80 per barrel for the first time since 2024, then jumped past $100 over the weekend.

Understandably, the price shock has left global financial markets contending with uncertainty around the conflict's duration and scope. Investors are asking familiar questions about inflation, economic growth and the trajectory of future Federal Reserve monetary policy.

The short answer to all of these questions is that the risks are real, yet history suggests it’s wiser for investors to focus on portfolio diversification than to react hastily to headline-driven volatility.

An extended conflict could amplify existing economic headwinds. For example, although estimates vary, a 10% rise in WTI crude prices typically lifts inflation (as measured by the Personal Consumption Expenditures Index) by one to two-tenths of a percentage point, all else being equal. The potential for inflation to rise adds risk for capital markets, as renewed price uncertainty could delay future Fed rate cuts—even as a more dovish Fed chair is set to take the helm in the coming months.

Even so, the U.S. economy is less vulnerable to energy shocks than it was in the past. Energy use relative to GDP has fallen for decades and the United States is now a net energy exporter. These structural shifts haven’t eliminated the risk of higher prices, but they should ameliorate to some extent the economic drag and inflationary impulse relative to prior cycles.

For added context on the economic effects of rising geopolitical tensions, listen to this recent podcast with Nationwide’s Chief Economist Kathy Bostjancic and Chief Investment Officer Chris Graham.

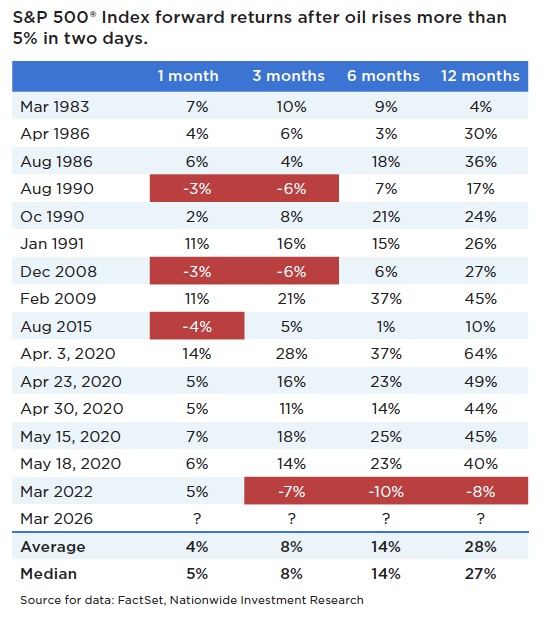

Investors should pay attention to the potential economic implications as events unfold, but history shows that markets have absorbed geopolitical oil shocks and recovered. In episodes where oil prices rose more than 5% over two consecutive sessions—as they did on March 2 and March 3—the S&P 500® Index went on to post average gains of 14% over the next six months and 28% over the following 12 months. (See the accompanying table.)

This pattern highlights the forward-looking nature of equity markets. Investors tend to look beyond near-term turbulence and focus on the longer-term earnings power of corporate fundamentals, which remain broadly resilient in the current environment. And while geopolitical uncertainty continues to cloud the outlook, recent economic data still point to a constructive backdrop—suggesting the U.S. economy entered this period with meaningful underlying strength. That context may matter more for long-term outcomes than the geopolitical event itself.

History also shows that investors who exit the market during geopolitical shocks often miss much of the rebound. For clients with well-constructed, diversified portfolios aligned with their goals and risk tolerance, the weight of evidence supports patience over emotional, headline-driven reactions.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.