Less bulls and bears, more market fundamentals

Key takeaways:

- Q1 earnings results continue to reflect resilience, with most companies exceeding expectations and remaining on track for a sixth consecutive quarter of double-digit earnings growth.

- Markets are ultimately shaped by underlying fundamentals, such as margin expansion, which has been a key contributor to recent market resilience.

05/06/2026 – Investors tend to gravitate toward narratives—especially when markets feel unsettled. During periods of elevated uncertainty, it’s instinctive to organize complexity into simpler, opposing outcomes—bull versus bear, optimism versus caution, conviction versus fear—to frame an otherwise ambiguous future.

While the desire for simplicity is understandable, it can also pull investors toward emotional decisions at exactly the wrong moments. In reality, markets are not a clash of competing outlooks; they are mechanisms for discounting a future stream of earnings. By that measure, the underlying signal is far clearer than the surrounding noise would imply.

Still, the bull-versus-bear debate continues to dominate the narrative, making it worth understanding both camps—if only to weigh the merits of each perspective. Stock market bears have no shortage of evidence to support their case: geopolitics remain unsettled; energy markets are volatile; the policy outlook is opaque; and the implications of artificial intelligence are evolving at a blistering pace. From their vantage point, investors have grown too comfortable rationalizing away the risk of macroeconomic shocks. In that scenario, they argue, earnings pressure would emerge gradually as forward guidance and earnings revisions ultimately force a reckoning.

The stock market’s sharp rebound in April—its best month since 2020—may bolster the bullish case, but bears are quick to counter that narrow leadership and persistent selling into rallies suggest conviction remains conditional rather than durable. The bullish counterargument, however, is not rooted in irrational exuberance or Pollyannaish forecasts. Instead, hard economic data remains broadly constructive, and the rebound from the March 30 low reflects more measured re-risking than speculative excess—underpinned by substantial fiscal and monetary support.

More importantly, earnings continue to do the work that narratives cannot. First-quarter results underscore the resilience of U.S. businesses, with most companies exceeding expectations and aggregate earnings growth tracking at a mid-teens pace. If realized, this would mark a sixth consecutive quarter of double-digit earnings growth—hardly a fragile backdrop for investors. Notably, forward estimates still point to positive earnings growth across every sector in 2026.

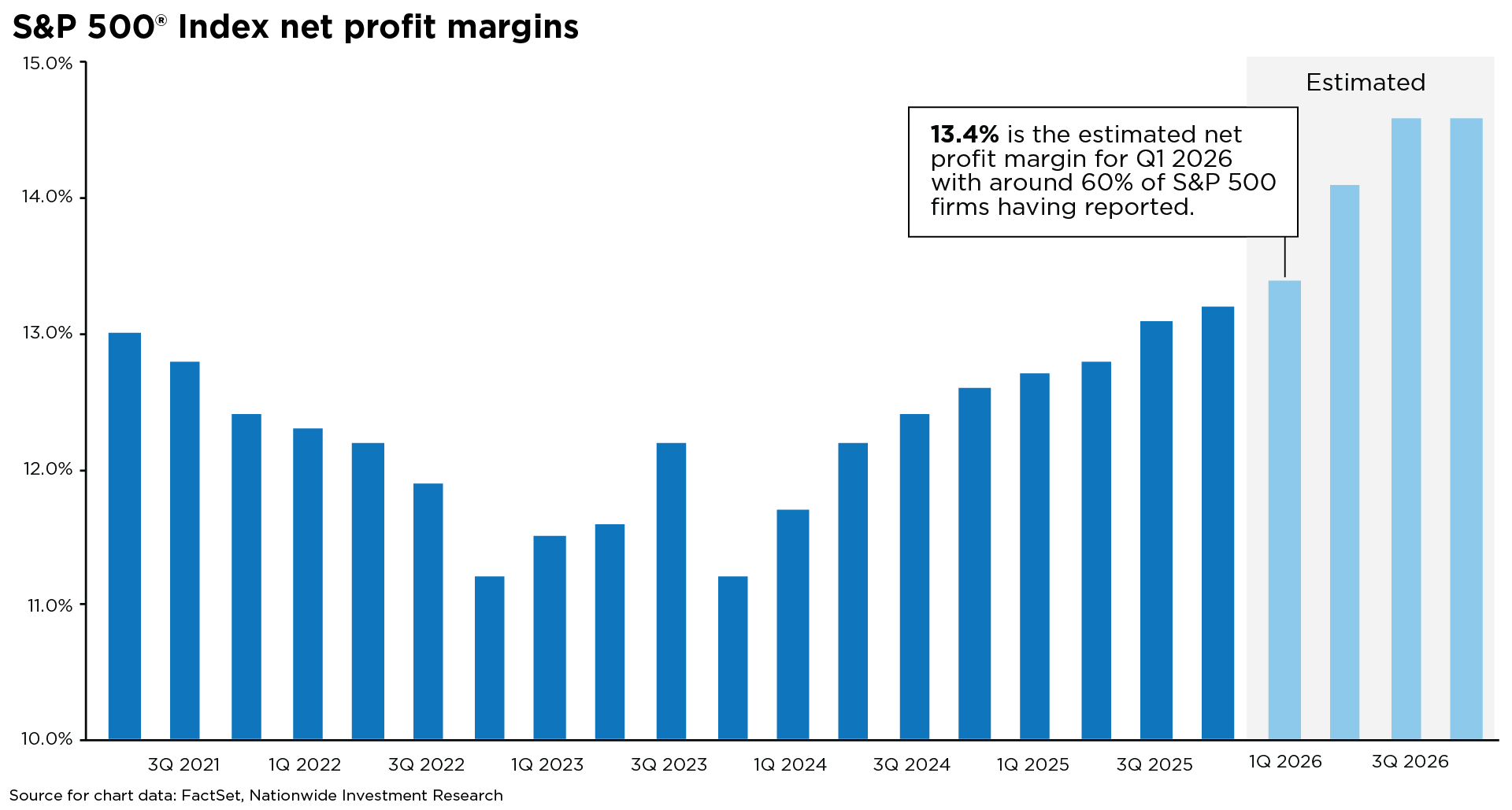

For investors, focusing on the bull-bear debate risks missing the forest for the trees. Markets are ultimately shaped by underlying fundamentals rather than prevailing narratives. With the S&P 500® Index, margin expansion has been a key contributor to recent market resilience. Margins are not merely holding—they remain a meaningful driver of equity market returns.

A ninth consecutive quarter of double-digit margin growth would push net profitability for S&P 500 firms to its highest level since tracking began in 2009. Consensus expectations call for further expansion in the back half of 2026. This persistence is not a statistical fluke; it more likely reflects a compositional shift within the S&P 500 as it evolves toward asset-light businesses with high operating leverage—where scale amplifies profitability rather than constrains it. Nowhere is this clearer than in the technology sector, which has not only driven revenue growth but has fundamentally raised margin ceilings, as illustrated by the economics of hyperscale platforms.

The bull-bear debate offers investors plenty of arguments to weigh, but it should not distract from the observable drivers of return. The persistence of elevated margins provides the clearest evidence that equity fundamentals remain durable—even against an unsettled macroeconomic backdrop.

Hear why equity markets have remained resilient amid geopolitical uncertainty—tune in to the latest Economic Insights podcast featuring Mark Hackett and Nationwide Chief Economist Kathy Bostjancic.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.