Why markets are rotating

without the fundamentals to match

Key takeaways:

- The gap between expectations and fundamentals is driving this rotation.

- Chasing rotations can add unnecessary risk.

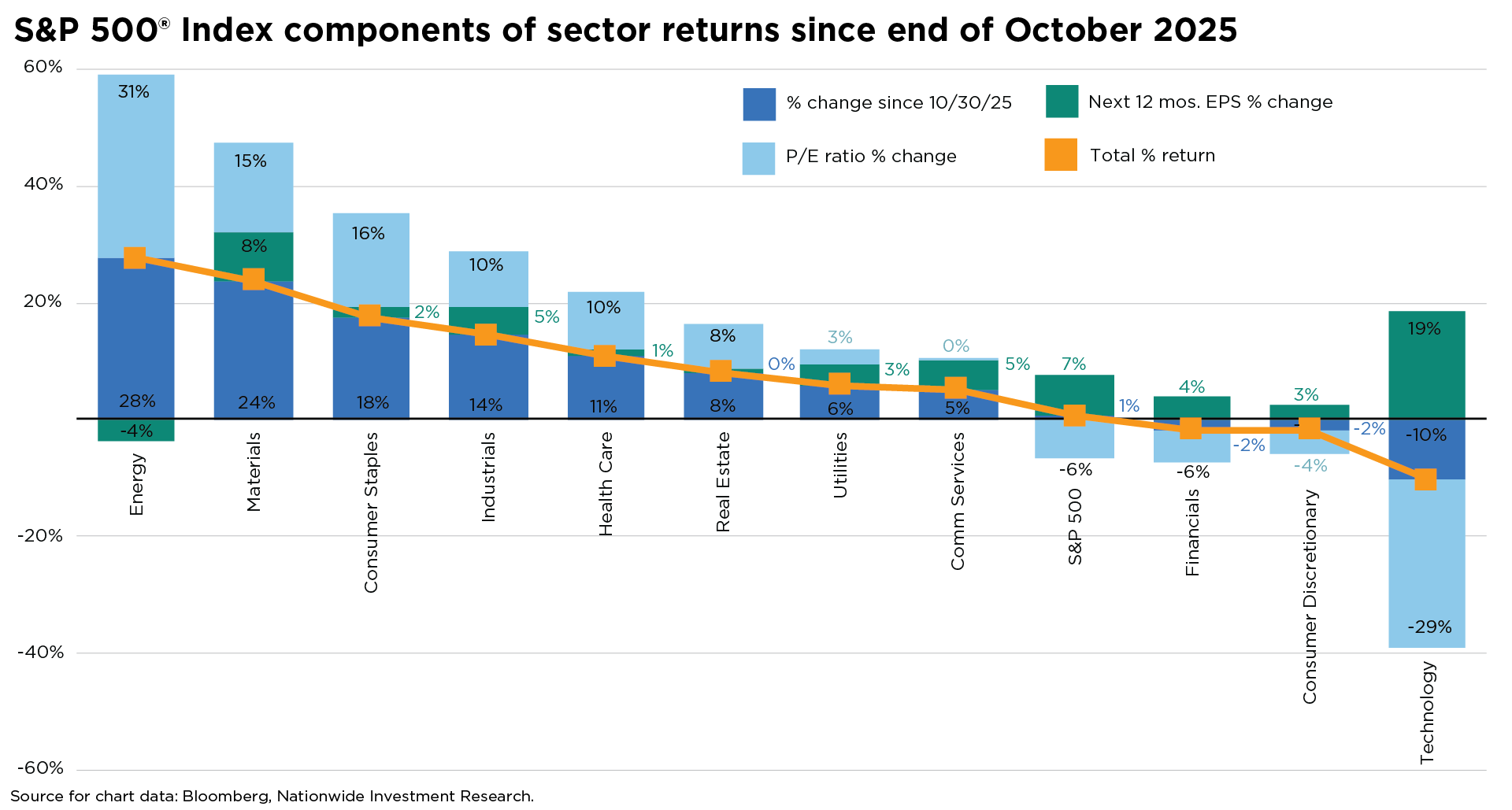

03/04/2026 – Since last October, sector performance has split sharply. Energy, industrials, health care, and materials have posted strong gains, while technology, consumer discretionary, and financials are down year-to-date. It’s a clear sign that price action and earnings trends have moved out of sync across the market.

This disconnect between expectations and fundamentals has shaped the rotation. It’s creating both opportunities and risks as long-standing correlations break down. Whether that gap closes or widens will be a key driver of sector leadership from here.

At first glance, the rotation looks logical—money is moving from pricey, AI-exposed growth into cheaper, real-economy sectors. But the earnings backdrop tells a different story. As of this writing, energy is up 27% since October as forward earnings have slipped nearly 5% and its forward P/E has jumped about 30%. Here, sentiment is clearly outpacing fundamentals.

That said, while the recent oil spike may look like it breaks the broader downtrend in crude, the historical pattern is more nuanced. Strategas finds that, on average, oil prices are lower three and twelve months after geopolitical conflicts begin—suggesting the current surge is likely temporary, even if near-term input costs and volatility remain a challenge in client conversations. A key indicator to watch is the Brent–WTI spread: a sustained widening would point to rising seaborne supply pressures and broader stress in global flows, helping determine whether the recent expansion in Energy’s forward P/E has a fundamentally durable basis.

Industrials show a similar pattern. The sector is getting a lift from policy support, deregulation, full-expensing incentives, and expectations for monetary easing—all of which have boosted sentiment ahead of the data. That enthusiasm has pushed valuations to a historically high 28x forward earnings despite 5% expected earnings growth, an unusual setup for a typically counter-cyclical sector.

This pattern is showing up across the broader market as well. Positioning and sentiment continue to outpace fundamentals, with price often signaling conviction before the data does. That tension helps explain why the S&P 500® Index has spent the past six months grinding sideways just below its highs.

Even as macro signals tilt toward a reflation trade, positioning remains a major driver of sector rotations. Back in October, capital was heavily concentrated in tech and other growth names, while cyclical sectors were largely avoided. As that crowding eased toward year-end, price moved first and the narrative followed—highlighting why investors should be careful not to overread stories after the fact.

Positioning and sentiment can often front-run fundamentals, and when they move together, price can project conviction before the data supports it. That tension between price-implied confidence and still-developing fundamentals sits at the center of today’s market and helps explain why the S&P 500 has hovered just below all-time highs.

As price action continues to drive the narrative in a market marked by elevated dispersion, investors may feel tempted to chase each new rotation. A more durable approach is to align portfolio positioning with long-term objectives and a risk/reward profile that can withstand shifting narratives and uncertain fundamentals.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.