Perception versus reality:

Conflicting signals in the markets

Key takeaways:

- The growing gap between investor sentiment and actual economic conditions has made many traditional market signals less dependable.

- A key risk today is drawing the wrong conclusions—treating shifts in sentiment or market moves, especially when they differ from economic data, as clear signals about where the economy is headed.

04/30/2026 – Geopolitical uncertainty dominated the stock market narrative for much of the first quarter, but it may ultimately be remembered less as a standalone shock and more as a reflection of deeper structural fragilities that have been building for years—showing up across sentiment indicators, economic surveys, and investor positioning.

Take consumer confidence, for example. Already under pressure from a range of economic headwinds, sentiment now appears set to collide with the heightened emotional volatility that often accompanies midterm election cycles. The result is an additional strain on an already fragile backdrop—one where investor psychology is becoming more reactive and less anchored, as evidenced by the recent whipsaw in the CNN Fear & Greed Index.

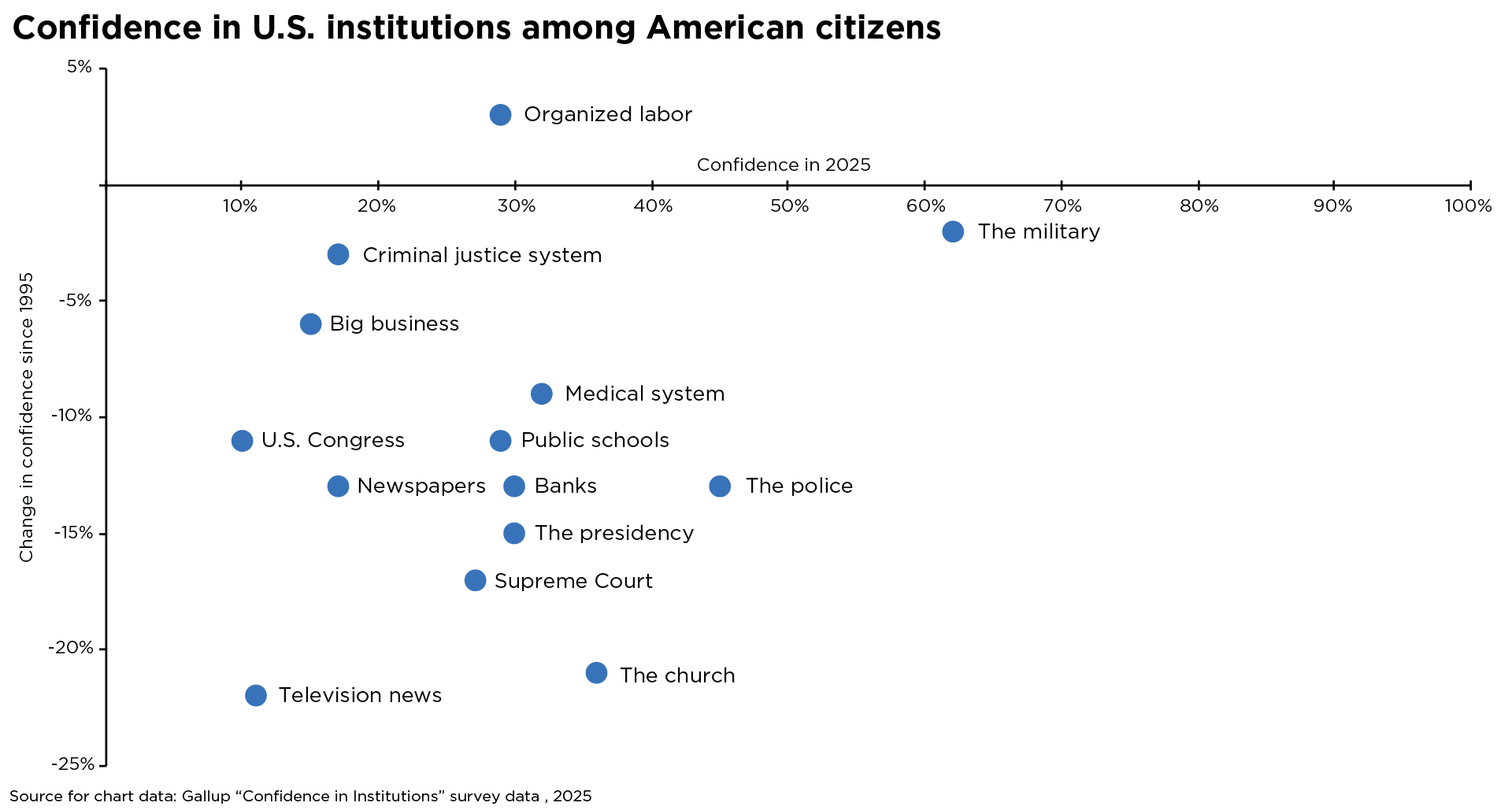

The gap between how investors feel and how the economy is actually behaving has defined this cycle, upending traditional signals and making once-reliable forecasting tools less dependable. Complicating matters, this disconnect is unfolding against a backdrop of already diminished institutional trust among U.S. citizens (see chart)—a dynamic that may leave some investors more susceptible to headline risk and rapid narrative shifts.

The result is a landscape defined by contradictions—where conflicting data, competing narratives, and unexpected market responses coexist. That tension has widened the range of outcomes and challenged the reliability of traditional frameworks used to assess risk and opportunity in the stock market.

This backdrop helps explain why consumer confidence, as measured by the University of Michigan Consumer Sentiment Index, can hover near historic lows even as equity markets push to new all-time highs. It may also shed light on why some parts of the economy appear close to contraction despite pockets of resilience, and why inflation perceptions vary so widely across measures. For example, market-based inflation expectations have remained relatively anchored, even as consumer-focused surveys have reacted more forcefully to inflationary pressures. Together, these trends underscore the widening gap between price-based market signals and survey-based sentiment.

In this broader context, survey-based measures may function less as objective signals and more as a form of emotional shorthand—bundling concerns about affordability, economic stability, and policy credibility into a noisy mix of outcomes. For investors, the real risk is not volatility itself but misattribution: treating sentiment surveys (soft data), market pricing, or their divergence from hard economic data as definitive signals about underlying macroeconomic conditions.

As we move through the rest of 2026, investors would be well served to remember that in periods marked by fractured signals and heightened emotion, clarity rarely comes from chasing louder narratives. More often, it emerges through patience, perspective, and staying invested through the cycle.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.