Stocks rebound fast—but can it last?

A familiar market question

Key takeaways:

- While market turning points often appear obvious only in hindsight, periods of peak uncertainty can give way to improving fundamentals with little warning. Some of the market’s strongest days have closely followed its weakest.

- Maintaining a long-term perspective does not require ignoring near-term risks; those risks should be kept in proper context and not allowed to drive emotional decisions.

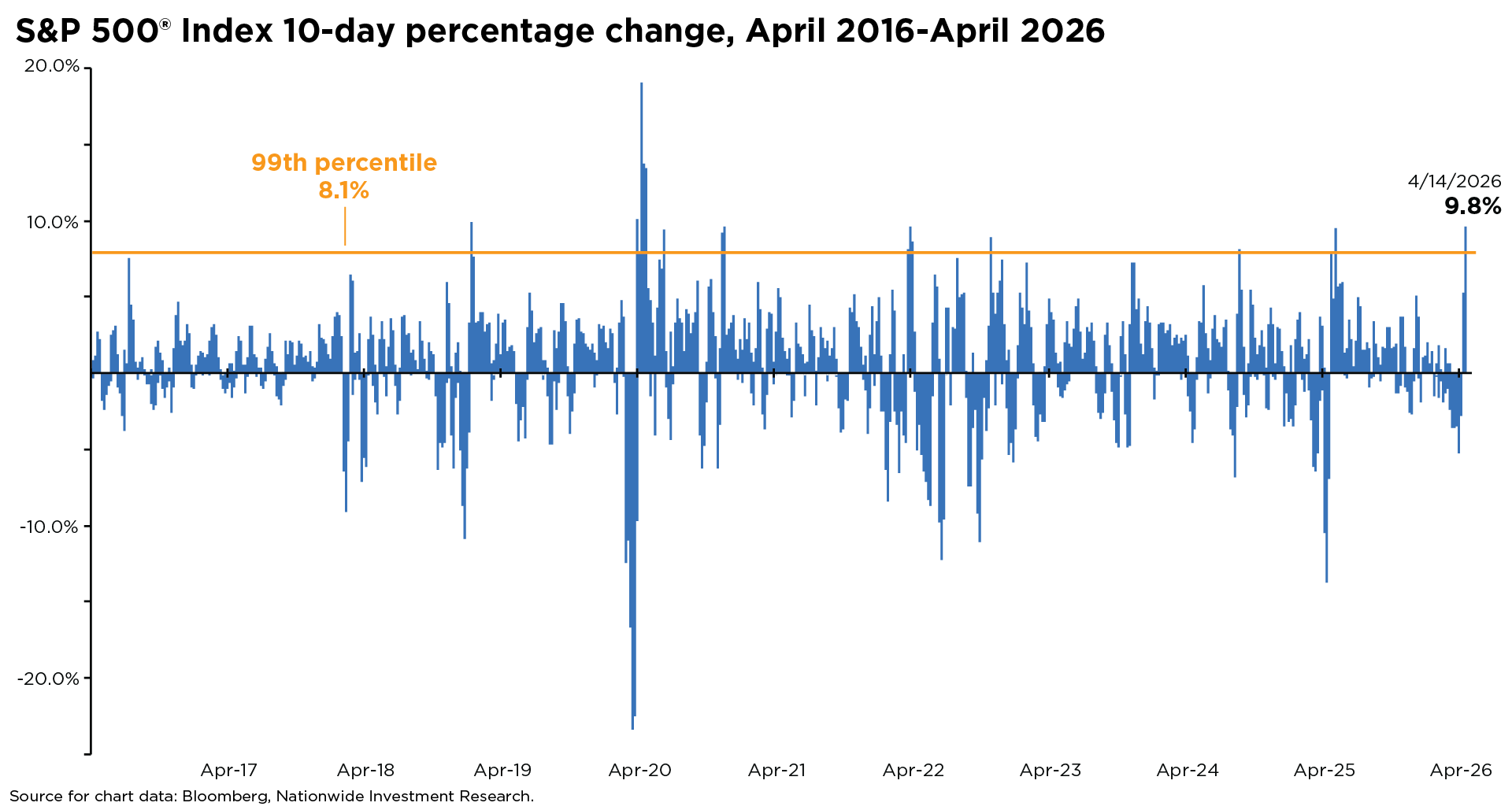

04/22/2026 – The stock market has once again demonstrated notable resilience this month, despite no shortage of headwinds. Over the 10 trading days through April 14, the S&P 500® Index advanced 9.8%, fully retracing the drawdown tied to the early weeks of the Iran conflict. That move places the rally in the 99th percentile of all 10-day advances since 1990 (see chart). Moreover, the S&P 500 has posted gains of roughly 3% for three consecutive weeks—a pattern that has occurred just twice in market history.

At face value, the move points to a market that is both durable and forward-looking, as investors quickly price in geopolitical risk rather than wait for full resolution. In the process of reasserting its upward trend, the S&P 500 reclaimed both its 50-day and 200-day moving averages in a single trading session in March—a rare technical reset that underscores how abruptly sentiment and positioning shifted.

The announcement of a two-week ceasefire between the U.S. and Iran marked a clear inflection point for sentiment and positioning, as the narrative shifted away from escalating tail risks toward more constructive scenarios. Against that backdrop, the equity rally was fueled less by new optimism and more by positioning dynamics: bearish investors unwound short positions, systematic strategies flipped from sellers to buyers, and hedge funds rapidly covered hedges to re-establish exposure.

Collectively, these moves amplified upside momentum despite ongoing uncertainty, underscoring that the rally has been driven more by market mechanics than by a meaningful resolution of the risks that initially pushed volatility higher. The speed of the rebound may also obscure a familiar pattern seen during periods of heightened uncertainty: outsized moves often cluster around inflection points that are only clear in hindsight. The takeaway is not that the rebound lacks credibility, but that its staying power will hinge on whether fundamentals can support higher valuations.

Encouragingly, the latest Bank of America Global Fund Manager Survey suggests valuations are no longer the overhang they were earlier this year, as the share of institutional investors who view U.S. equities as overvalued fell to its lowest level since February 2019. At the same time, if corporate results prove resilient in the upcoming earnings season, the move could evolve into a more sustained advance. Crucially, that outcome does not require risks such as geopolitical conflict to be fully resolved. Equity markets have often moved higher even as uncertainty persists, with market bottoms forming well before geopolitical conflicts reach clear resolution.

Similarly, the recent rally highlights a familiar—but often misunderstood—dynamic that can get lost amid market volatility: markets tend to turn not when uncertainty is fully resolved, but when the rate of change begins to improve. The unwind of deeply bearish positioning amplified that shift, producing an outsized rebound even as geopolitical and economic risks persisted. While further gains will depend on whether fundamentals can validate current prices, history suggests periods of peak uncertainty often coincide with the early stages of recovery.

The speed of the recent rebound also illustrates why market timing remains challenging. While turning points appear obvious in hindsight, periods of peak uncertainty can give way to improving fundamentals with little warning. In fact, some of the market’s strongest days have occurred shortly after its weakest.

For investors, history shows that a long-term perspective does not require ignoring near-term risks. Those risks should be kept in proper context—not allowed to drive emotional investment decisions. While volatility may persist, the broader fundamental backdrop—including rising earnings expectations, durable AI-related investment, and fiscal support—remains intact.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.