Q1 volatility pressured markets,

but fundamentals held firm

Key takeaways:

- Last quarter’s market pullback reflected pressure on valuation multiples—not deteriorating fundamentals—as higher crude prices and rising geopolitical tensions challenged investor confidence in the economic outlook.

- Looking ahead, forward guidance in Q1 earnings reports should be especially informative as investors assess margins, pricing power, and the durability of earnings momentum.

04/15/2026 – The first quarter of 2026 may be remembered less for the headlines themselves and more for how markets absorbed them. Investors faced a steady accumulation of pressure: surging energy prices, higher interest rates, a rapid reset in monetary expectations, and lingering concerns around private credit. Yet the adjustment played out in a measured—if uncomfortable—way, underscoring the market’s capacity to digest stress without systemic disruption.

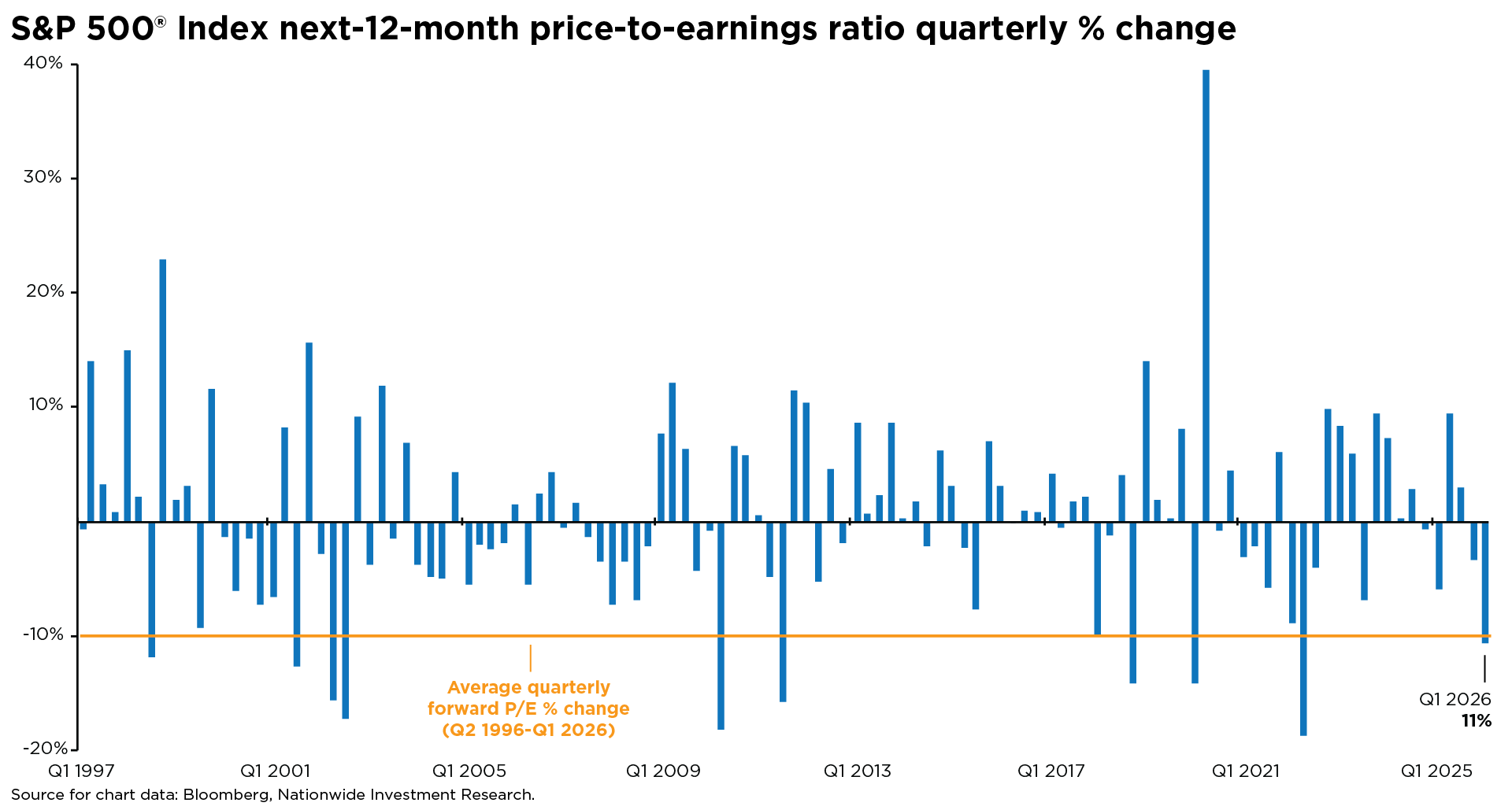

As investor sentiment wavered during the quarter, the S&P 500® Index fell roughly 9% from its January all-time high. The pullback was a grinding descent, driven less by weakening fundamentals and more by a market struggling to sustain valuation multiples as crude prices surged above $100 and geopolitical tensions clouded the strong economic backdrop investors had relied on at the start of the year.

By late March, the S&P 500’s forward price-to-earnings multiple had compressed by roughly 18%, falling from about 23 times next-twelve-month earnings in October to near 19 times by March 23rd. The multiple subsequently rebounded toward 20 times after reports of a two-week ceasefire in Iran eased the geopolitical risk that had weighed on markets since late February.

While geopolitical developments dominated investor attention, the valuation adjustment unfolded in two distinct phases. The first emerged in February, as markets reassessed what the next stage of AI disruption could mean for terminal values across select technology segments. Those concerns pressured P/E multiples even before geopolitical tensions escalated. Underpinning the bearish case was a broader view that neither valuations nor labor market conditions fully justified the market’s earlier upward trajectory.

As the quarter progressed, both pillars of that argument began to weaken. The labor market proved more resilient than expected, while valuation concerns eased as AI disruption prompted a sharp de-rating across select software names and the broader technology complex.

The second phase unfolded as a broader geopolitical risk premium weighed on equities, amplifying multiple compression as crude prices surged and uncertainty eroded investor confidence. Critically, neither phase of the adjustment was driven by earnings deterioration—a crucial distinction. The market’s P/E multiple contracted by roughly 12% over the first quarter, ranking among the 10 sharpest quarterly compressions of the past three decades, even as fundamentals continued to move in the opposite direction.

Consensus forecasts for 2026 earnings increased steadily throughout the quarter, rising by roughly 300 basis points—from about 14% expected growth at the start of the year to approximately 17.4% as of this writing. Another quarter of double-digit earnings growth would mark six in a row, reinforcing the view that the Q1 selloff reflected a valuation reset rather than a breakdown in fundamentals.

Looking ahead, the key question is not the backward-looking earnings results themselves, but the guidance and management commentary that accompany them. Those signals should prove far more informative in assessing margins, pricing power, and the durability of earnings momentum—particularly if elevated energy prices continue to pose a risk to economic growth.

Author(s)

Mark Hackett, CFA®, CMT®, CFP®

Chief Market Strategist, Nationwide Investment Management Group

Mark Hackett is the Chief Market Strategist for Nationwide’s Investment Management Group, bringing more than 20 years of experience in the asset management industry to the role.

Trending articles

In the coming years, more people will begin to think about the costs of health care in retirement and the possibility of needing long-term care (LTC) in the future, especially as the number of Americans reaching age 65 hits an all-time high this year.

Considerations for financial professionals on supporting retirees through economic uncertainty.

This guide explores strategies for securing long-term care for children with special needs through special needs trusts, ABLE accounts, and government benefits.