Medicare premiums increase in 2026: How to help your clients’ planning

Key takeaways

Health care is one of the largest and most unpredictable expenses in retirement, with Medicare premiums that include prescription drug coverage one of the biggest costs. In 2026, Medicare will see one of the steepest Part B premium increases in recent years, along with higher deductibles and higher premiums for prescription drug coverage. This means that this year, your guidance as a financial professional is needed more than ever.

Let's look at the Medicare changes for 2026 and how you can help your clients prepare for them.

Medicare Part B premiums for 2026

Part B covers doctor visits, outpatient services and many preventive care benefits. In 2026, both premiums and deductibles will rise sharply.

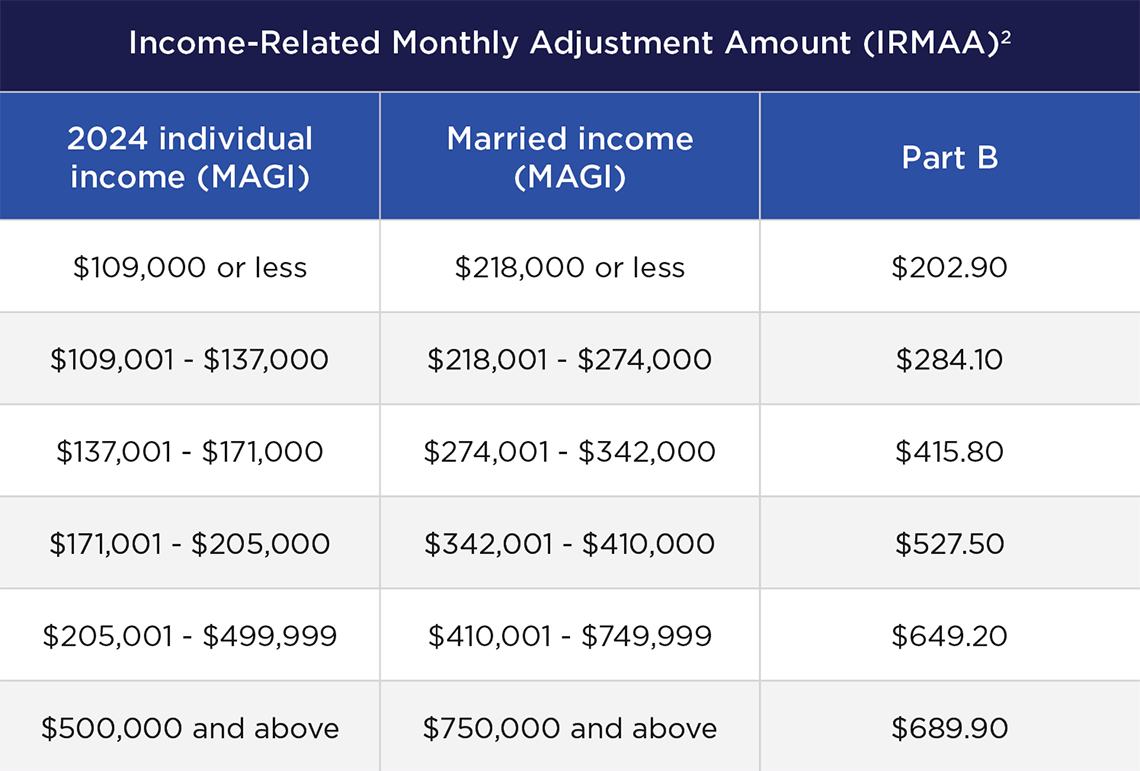

Finally, keep in mind that higher-income individuals must pay the income-related monthly adjustment amount (IRMAA), which is a surcharge to their Part B premium. In 2026, a couple who earned between $342,001 and $410,000 in 2024 will pay an additional $527.50 per month for their Part B premium.2

Medicare Part D cost changes for 2026

Part D covers prescription drugs through private plans approved by Medicare. Considering that 87% of people ages 65 to 74 use prescription drugs, this is a key cost to watch for retirement planning.4

In 2026, Medicare beneficiaries will see a combination of higher costs and continued caps on prescription drug prices:

Medicare Advantage

Medicare Advantage plans vary by insurer and type of plan. For 2026, the Centers for Medicare & Medicaid Services (CMS) report that monthly premiums across Medicare Advantage plans will decrease from $16.40 to $14. However, enrollees may find higher pricing across many of the larger insurers’ plans.

CMS also projects that enrollment in Medicare Advantage will fall for the first time in two decades to 34 million from 35 million in 2025. Historically, half of enrollees leave their Medicare Advantage plans within 5 years. The top reasons for leaving, however, typically involve difficulty accessing care and dissatisfaction with care quality — not cost.

Medicare Advantage open enrollment is January 1 to March 31, 2026. During this time, individuals already enrolled in a Medicare Advantage plan can switch to a different Medicare Advantage plan or return to Original Medicare and enroll in a separate Part D drug plan. However, switching from Medicare Advantage to Original Medicare could result in being denied Medigap coverage (or effectively denied by being priced out), meaning a Medigap insurer can deny coverage or charge higher premiums based on pre-existing conditions and medical underwriting. This would have the effect of making the switch back to Original Medicare not financially feasible.

How higher Medicare costs impact retirement budgets

Rising Medicare costs can have a ripple effect across every part of a client’s retirement plan. Even modest annual increases can translate into meaningful lifestyle adjustments over time. Taken together, Medicare cost increases can:

- Reduce discretionary spending: As more income goes toward health care, less may be available for travel, leisure or family gifting; clients may need to reassess spending priorities and adjust lifestyle expectations to maintain financial stability

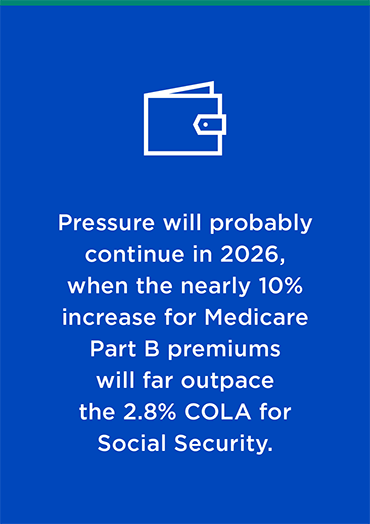

- Put pressure on fixed incomes: Retirees who rely primarily on Social Security or fixed pensions may feel an even greater squeeze because higher premiums and deductibles have outpaced Social Security’s yearly cost-of-living adjustments (COLA), eroding purchasing power year after year; this will probably continue in 2026, when the nearly 10% increase for Medicare Part B premiums will far outpace the 2.8% COLA for Social Security

- Increase tax exposure: For higher-income retirees, IRMAA surcharges can add hundreds of dollars per month to Medicare premiums; strategic income planning — such as when to take withdrawals or complete Roth conversions — can help reduce exposure and preserve more of what clients have saved

- Amplify long-term inflation risk: Health care inflation has historically risen faster than general inflation; to avoid underfunding, it’s important to model annual increases of 5% to 6% for health care costs rather than relying on general inflation assumptions

Planning strategies for financial professionals

Educate clients on IRMAA thresholds and tax planning:

Explain to clients how income affects Medicare premiums. Review strategies such as Roth conversions or withdrawal timing to reduce exposure. Nationwide’s Tax Planning Quick Reference Guide can help.

Schedule Medicare planning reviews:

Meet with clients age 60 and older to discuss upcoming changes, review their coverage options and plan ahead for enrollment windows.

Evaluate Medicare plan trade-offs:

Help clients weigh the pros and cons of original Medicare versus Medicare Advantage, including potential hidden costs and network limitations. Many clients are drawn to “zero premium” Advantage plans, but limited provider networks and care access issues often lead to disenrollment.

Update retirement projections: Incorporate 2026 Medicare costs into client plans and model future increases, using 5% to 6% annual health care inflation rather than general inflation

Encourage clients to invest for the long term: As a hedge against rising costs, suggest that clients keep a portion of their portfolio invested in assets with the potential to outpace health care-related inflation.

Help clients plan with confidence

Medicare is one of the biggest drivers of your clients’ long-term costs during retirement. With premiums and deductibles heading higher in 2026, the stakes are rising for retirees who want to protect their lifestyle and preserve their savings.

Your guidance can make the difference between a post-retirement financial plan that strains under unexpected health care expenses and one that adapts smoothly. By helping clients understand what’s changing, modeling the impact on their budgets and building strategies to manage costs, you show the real value of working with a financial professional who looks at the whole retirement picture.