Supporting charitable causes while protecting children’s inheritance

A charitable gifting plan can enable your clients to create a meaningful and lasting legacy as they make a significant contribution to their community and take advantage of financial benefits for themselves and their family members. For you, exploring charitable gifting options with clients can deepen your relationship with them as you lay the groundwork for business relationships with their heirs.

What gifting options are available?

There are many strategies for charitable gifting, each generally offering tax benefits to the person making the gift. Those benefits vary based on the nature of the asset gifted and the strategy used. The many ways to execute on charitable intent include, but are not limited to:

What are the benefits and how does it work?

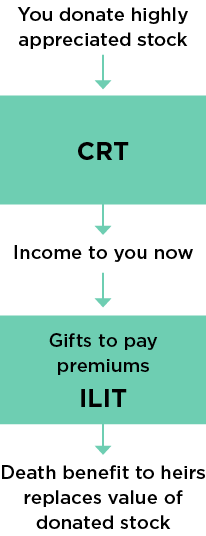

What about the children?

When considering support for charity, one potential issue arises regarding its impact on the inheritance of the clients’ children. After all, if they make large donations to charity, there will be less to pass on to heirs.

By proactively planning to replace the value of their donation, they can skirt this issue with an irrevocable life insurance trust (ILIT) — a wealth replacement trust.

They use the income from the CRT to make gifts to the ILIT, which can then purchase a life insurance policy on them.

When they pass away, the tax-free death benefit will pay into the trust. The trust will then distribute the tax-free death benefit to their heirs.

Additionally, they can use the trust to control the distribution of the death benefit through restricted beneficiary designations. This can be a useful consideration when heirs may be too young or immature to handle a lump-sum inheritance.