Estate equalization for high net worth clients

Key highlights

Life insurance death proceeds can be used to equalize an estate that has highly valuable and/or hard-to-divide assets.

An example

Ruth, 67, is a recent widow. Ruth has a sizable estate and is concerned about federal estate and other inheritance taxes. She and her husband raised 3 children in an elegant family home on the East Coast. Rachel, 43 and the oldest of her children, is single with a successful career in Chicago. She is settled into her life and has no desire to move back east. Brenda, 41, is the middle child and is married to Adam. Together with their 3 children, they live close to Ruth in what they like to call their “forever home.” Dan, 38, is the youngest, and he also lives close to his mother. Dan studied hospitality in college and works at a nearby hotel that is quite popular with tourists. He has expressed his desire to someday convert his parents’ home into a bed-and-breakfast. He is married to an interior designer and feels confident that the mix of his hospitality skills and his spouse’s good taste would help them create a successful and inviting business.

Ruth loves Dan’s enthusiasm for keeping the house in the family and converting it into a bed-and-breakfast. She plans to leave the property to him, but the value of the family home is more than 50% of the value of her total estate.

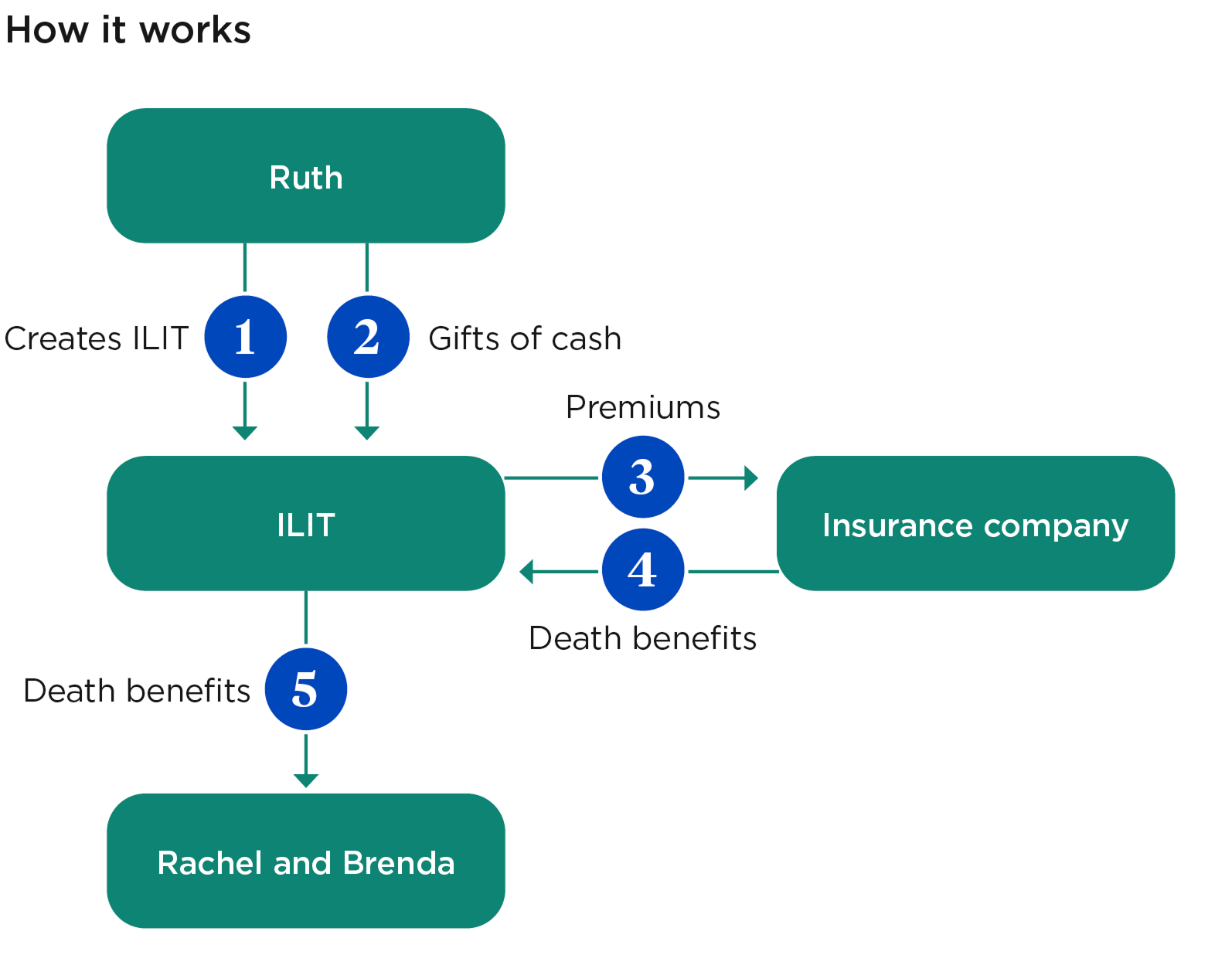

Estate equalization steps

- Ruth sets up an ILIT with Rachel and Brenda as trust beneficiaries and makes cash gifts to the trust.

- The ILIT purchases life insurance on Ruth's life such that the trust receives the death proceeds at Ruth's death to pay to Rachel and Brenda, which creates equity in the overall distribution of the estate.

- The premium payments paid by the ILIT are not deductible, but when Ruth passes away the death proceeds paid to Rachel and Brenda are generally income tax free.

Cautions

If properly drafted, an ILIT can allow the trustee access to the accumulated cash value of the life insurance policy by taking loans on the cash value earnings and/or distributions of the cost basis — even while the insured is alive. If, however, the death proceeds remain in the trust after the death benefit has been paid, any investment income that is earned and not distributed to the beneficiaries may potentially be taxed at higher trust tax rates.

An ILIT is an irrevocable trust, which generally means no changes can be made once the trust is finalized. As a general rule, whatever is put into the trust is no longer accessible, and this could have serious implications if circumstances change. For example, if a grantor puts a house or a significant amount of cash in the trust with the intent that it will be given to their heir, and then the grantor unexpectedly needs those assets in the future, the grantor generally cannot obtain them. In some cases, an irrevocable trust can be dissolved, redacted or decanted into a new trust if allowed under state law. Refer clients to a trust attorney in their state of residence.