Loading...

Funding a trust with nonqualified deferred annuities

Key takeaways

There is an opportunity to use nonqualified deferred annuities as a funding vehicle for an existing credit shelter trust arrangement, or other irrevocable trusts that were established and funded in the past.

NQ deferred annuities can help minimize income taxes paid by the trust during a surviving spouse’s lifetime, as well as minimize the potential impact of the 3.8% Medicare surtax

Another funding option is life insurance; NQ deferred annuities may be advantageous in the case of the surviving spouse being uninsurable, or insurable only at exorbitant rates.

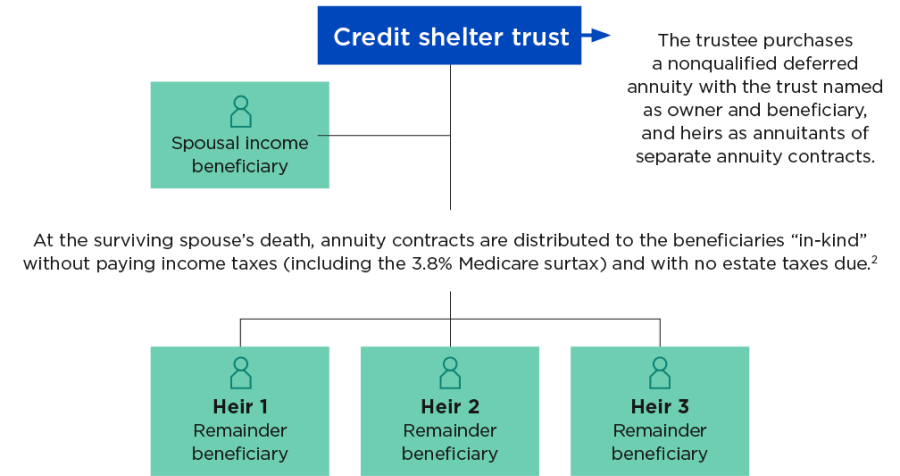

Trusts are an essential part of legacy planning, and funding a trust with a nonqualified deferred annuity may be an option. A common scenario is one in which a spouse dies and leaves assets to the surviving spouse in the form of a credit shelter trust (also known as a bypass trust, A/B trust or “B” trust). In this scenario, the surviving spouse does not need the income generated by these trust assets. But if the trustee leaves the income in the trust, the trust is on the hook for taxes that could be as high as 40.8%. (The top trust tax bracket is 37% + a 3.8% Medicare surtax, if applicable.) The trustee wants to avoid the trust paying tax, but does not want to make a distribution of the income out of the trust. So, what can be done to avoid the trust paying tax on the income?

An example

In 2017, Reggie Milton passed away and a credit shelter trust was funded with assets worth $5,490,000, which was equal to his available Applicable Exclusion Amount for federal estate tax purposes. Reggie’s surviving spouse, Roberta, is the income beneficiary of the trust, and their children, Roger, Renee and Rosa, are remainder beneficiaries in equal shares. Roberta does not need the income generated by the trust assets; thus, the trust is subject to significant income taxes as well as the Medicare surtax.

Solution

The trustee uses the trust assets to purchase three NQ deferred annuity contracts. Roger is named annuitant on one annuity contract, Renee on the second, and Rosa on the third. The trust is named as owner and beneficiary of all three contracts. Because all the trust beneficiaries are natural persons, the annuities should fall under the exception to the non-natural owner rule, and annuity gain is tax deferred.1

Upon the trust’s termination, or if the trust provisions allow distributions in-kind to the children, the NQ deferred annuities can be transferred from the credit shelter trust to the children without triggering gift or income taxes.2 Thereafter, the annuities will remain income tax deferred until the death of the respective owner/annuitant, or until voluntary distributions are made from the contracts.

We know that by using NQ deferred annuities in the trust, the trustee will be able to take advantage of several of the benefits and features provided by these contracts. In addition, using NQ deferred annuities as funding vehicles in a trust also provides:

- Tax deferral on annuity growth1: Any growth produced by the NQ deferred annuity contracts will remain tax deferred until distributions are made from the contract,3 whereas if the assets are invested in mutual funds (or some other taxable instrument), income taxes and the Medicare surtax may come into play.

- Distributions during the surviving spouse’s life3: The surviving spouse has a right to receive the income and often has a right to receive the principal (under certain limited criteria) from the trust. The trust may name all of the children as beneficiaries of the trust to receive distributions for any reason. As long as distributions of taxable income from the NQ deferred annuity are distributed to a trust beneficiary in the same calendar year, the trust will not pay income tax on the distribution. The beneficiary will pay income taxes on the taxable income at the beneficiary’s tax rate.3

Please consult with a tax advisor regarding application of the additional 10% premature distribution tax (10% tax) on taxable distributions from a deferred annuity owned by a trust. In PLR 202031008, the IRS ruled the 10% tax applies to taxable distributions from a deferred annuity owned by a non-grantor trust, with no allowable exceptions.

Cautions

- All of the credit shelter trust beneficiaries MUST be natural persons. For the annuity to be considered as tax deferred, it is generally recommended for all of the trust beneficiaries to be natural persons. However, please consult with your tax advisor for a determination.1

- In order to avoid the additional 10% premature distribution tax, the remainder beneficiaries of the trust should plan to defer taxable distributions of income from the NQ deferred annuity until after age 59½ or intend to pass the NQ deferred annuity assets to their own heirs.3

- When trust assets are sold to purchase NQ deferred annuity contracts, any gain may be taxable income to the trust, or the trust beneficiaries (if the taxable income is distributed to those beneficiaries), in the year the trust assets are sold.

- An important taxation issue to consider is the application of the additional 10% premature distribution tax (10% tax) on taxable distributions from a deferred annuity owned by a trust. In PLR 202031008, the IRS ruled that if a trust is a revocable or irrevocable grantor trust, the age of the individual grantor is used to determine application of the 10% tax. However, upon the death of the individual grantor, or for any non-grantor irrevocable trust, the IRS ruled that the 10% tax is paid by the trust on all taxable distributions from a deferred annuity owned by the trust.

Please note: PLRs are not considered as precedent-setting authorities and are binding only on the parties that requested the ruling, but they are an indication of the IRS opinion on a particular tax issue. When contemplating the purchase of a deferred annuity in an irrevocable non-grantor trust that will be taking distributions from the annuity, the trustee of the trust should obtain the opinion of a tax advisor to understand the potential consequences and risks of such a strategy.

[1] IRC Sec. 72(u)(1), PLR 9752035.

[2] PLR 199905015.

[3] Taxable distributions must fall within the scope of one of the exceptions to the premature distribution penalty under IRC Sec. 72(q). One of the most commonly used exceptions is for distributions to a person over age 59½. Because a trust does not have an age, this exception may never apply to distributions from an annuity contract owned by a trust. See PLR 202031008, and consult with a tax advisor regarding application of the additional 10% premature distribution tax to distributions from a deferred annuity owned by a trust.

Related topics & resources