Key takeaways

How guaranteed income drives retirement satisfaction

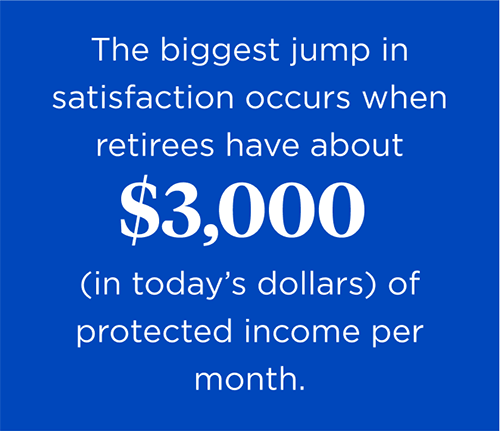

Our research uncovered a clear connection between the amount of guaranteed income a retiree receives and their overall retirement satisfaction. We analyzed data from the Health and Retirement Study (HRS) — a survey of approximately 20,000 older Americans conducted through the University of Michigan1 — and what we saw revealed that while any level of guaranteed income that supplements Social Security benefits improves confidence, the biggest jump in satisfaction occurs when retirees have about $3,000 (in today’s dollars) of protected income per month. This threshold creates an income floor that allows retirees to spend more freely without the fear of depleting their savings.

Interestingly, the positive effects of guaranteed income persist across nearly all wealth levels, excluding only the lowest net-worth tier. Even high-net-worth retirees report greater happiness and financial peace of mind when they receive approximately $3,000 in additional guaranteed monthly income. And as retirees age, their satisfaction with lifetime income sources only increases.

This impact is particularly strong among retirees age 70 and older. At this stage in life, the appeal of managing withdrawals and market fluctuations diminishes, while the simplicity and reliability of guaranteed income become increasingly valuable. This age-related trend suggests that clients who reach retirement without sufficient protected income may experience rising financial anxiety as they age.

Why guaranteed income matters

In a recent survey, more than 70% of millennial and Gen X respondents said they’re interested in learning more from a financial professional about how to set up their own protected retirement income.2