Why Social Security optimization planning matters

The age at which clients start claiming Social Security can have a huge impact on the size of their benefit. Clients can file as early as age 62, but they would receive a reduced monthly benefit compared with the amount they’d receive at full retirement age. Or they could delay filing up to age 70 to increase their monthly benefit by as much as 80%.1

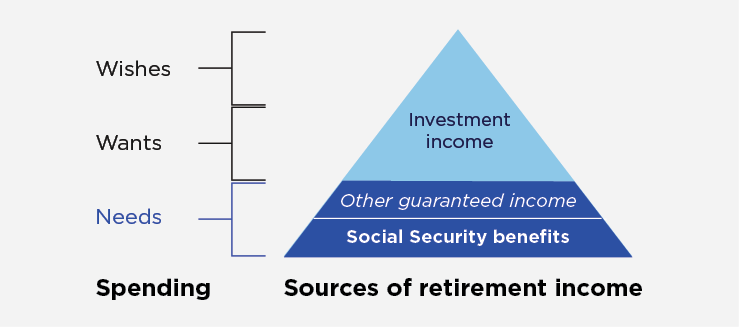

A guaranteed income floor

Social Security benefits are guaranteed income, so they provide an income floor in retirement. Benefits replace, by many estimates, about 30% to 40%2 of a retiree’s pre-retirement income from wages, with the remaining 60% to 70% of their monthly “paycheck” often coming from savings.

Unique benefits of Social Security

By itself, Social Security would be a powerful asset in a portfolio, and it offers features that other sources of income typically do not, including:

How current events affect Social Security claiming decisions

Client knowledge gaps and misunderstandings that hinder the ability to maximize benefits

Strategies for integrating Social Security benefits into an overall retirement income plan

Check out our videos

Learn how Nationwide can help you more confidently answer your clients when they ask: “When should I file for benefits?”