Minimizing taxes on Social Security benefits

Key highlights

Your clients may dislike taxes even more now than they did just a few years ago. According to a recent Gallup study, attitudes about federal income taxes in the U.S. are the worst in about 20 years. 6 in 10 Americans think their taxes are too high, according to the study. That’s up 3% from 2024 and 13% higher than in 2020.1

As a financial professional, this gives you an opportunity to provide a service that’s not only critical to your clients’ financial success but also highly valued by them: helping to minimize their tax burden. In fact, 2 out of every 3 affluent individuals say tax knowledge tops the list of important considerations when selecting a financial professional.2

There are a lot of ways to help clients plan for taxes in retirement. Many investors don’t understand that income taxes could be their single largest expense after they retire. You can provide valuable guidance by educating them on this fact and helping them implement strategies to minimize the expense. A great place to start is with the foundation of their retirement income: Social Security benefits.

Case studies: Diversified income sources can reduce tax burdens

Where retirement income is drawn from makes a big difference in how much of a client's Social Security benefits are taxed (or even if they’re taxed at all). Let’s explore case studies of 2 retired couples.

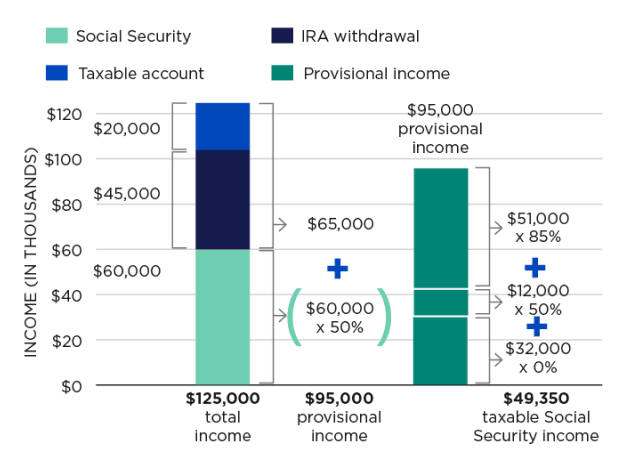

Couple 1

Both in their early 70s, married and filing taxes jointly, they want income of just over $10,000 per month ($125,000 per year). Their combined Social Security benefits fulfill about half of that, so they draw from 2 other sources:

$60,000 combined Social Security benefits

+$45,000 traditional IRA (ordinary income)

+$20,000 taxable account (long-term capital gains)

=$125,000 annual pre-tax income

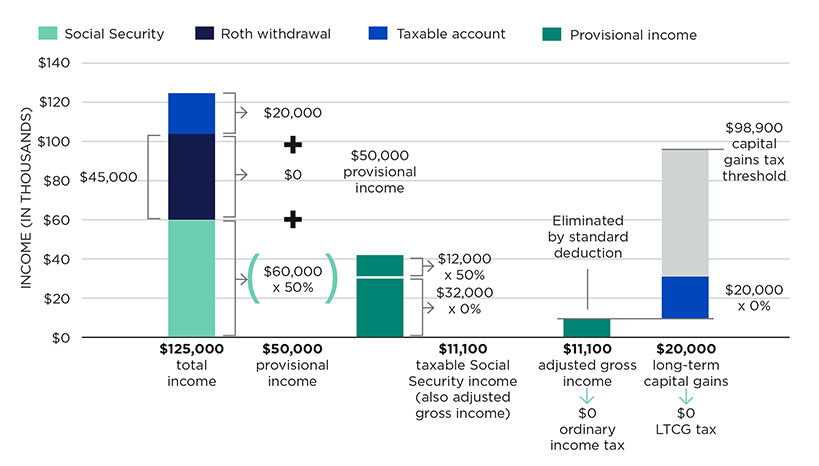

Couple 2

These folks are also both in their early 70s, married and filing taxes jointly. They too want income of just over $10,000 per month ($125,000 per year). Their combined Social Security benefits fulfill about half of that, and so they draw from 2 other sources:

+$45,000 Roth IRA (not taxable)

+$20,000 taxable account (long-term capital gains)

=$125,000 annual income (no income taxes owed)

A Roth IRA conversion allows your clients to move money from a traditional IRA into a Roth IRA. While the conversion itself is a taxable event, future withdrawals from the Roth IRA in retirement are tax-free and don’t contribute to Social Security provisional income.

By carefully balancing withdrawals from taxable accounts, such as brokerage accounts, and tax-deferred accounts, such as traditional IRAs and 401(k) accounts, you can manage your client’s adjusted gross income to keep it below the threshold at which Social Security benefits would be taxed.

HSAs can provide a triple tax benefit. Contributions are tax deductible, growth is tax free, and withdrawals for qualified medical expenses are tax free. After age 65, HSA funds can be withdrawn for any reason without penalty, although income tax applies to nonmedical withdrawals. Importantly, tax free withdrawals don’t count toward provisional income.

Encourage clients to invest in tax-efficient strategies such as cash value life insurance or using index funds, ETFs or tax-managed funds in taxable brokerage accounts. These can help provide income that is either not taxed or taxed at reduced rates, keeping the client’s overall income lower and potentially reducing taxes on Social Security benefits.

For clients who have other income sources, delaying Social Security benefits can sometimes result in larger levels of lifetime benefits and lower overall taxable income earlier in retirement. However, the decision to delay benefits should be balanced against the client’s overall financial picture and life expectancy.

For clients who are charitably inclined, qualified charitable distributions (QCDs) from an IRA can satisfy required minimum distributions (RMDs) while excluding the distribution from income, potentially reducing the tax on Social Security benefits.