Shockproof retirees’ income plans

Key takeaways

Some retirement expenses are expected. Others come as a surprise. And it’s those expenses, especially the big ones, that can throw a retirement income plan off course.

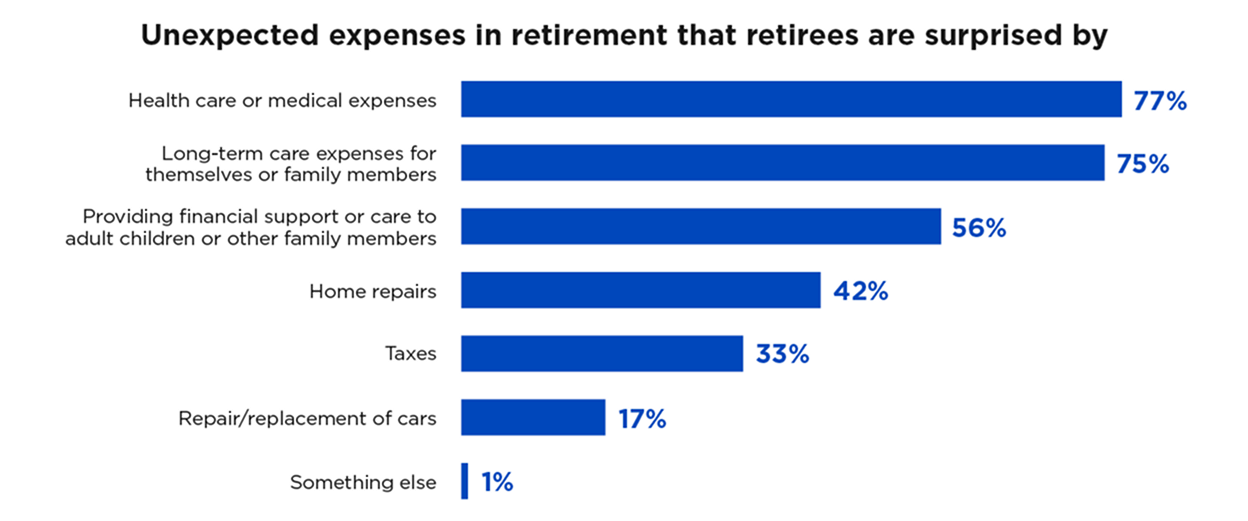

In fact, a recent survey found that 3 out of 4 financial professionals say their clients are often surprised by large health care or long-term care expenses in retirement.1 Unexpected medical bills, long-term care needs and support for family members all rank high on the list of spending shocks — expenses that can quickly drain resources and disrupt even a well-structured retirement income plan.

Understand the potential consequences

The problem with spending shocks isn’t just that they’re unexpected. It’s that many retirees don’t have a plan for how to pay for them.

When there’s no clear strategy, clients may pull from the easiest source of cash — often a tax-deferred account. But doing so without thinking through the tax impact can lead to unintended outcomes such as jumping into a higher income bracket, triggering higher taxes on Social Security benefits or increasing Medicare surcharges.

That’s why conversations about spending shocks should happen early and often. When clients understand that these events aren’t just possible but likely, they’re more willing to explore strategies that make it easier to handle them without creating new problems.

"Inflation is (finally) hitting health care," advisory.com/daily-briefing/2022/08/30/healthcare-costs (March 18, 2023).

Strategies to tackle unforeseen retirement expenses

A personalized combination of these planning strategies can help clients better prepare for unexpected costs:

- Build a recurring level of surplus retirement income compared with anticipated retirement expenses

- Review insurance coverage and help identify gaps that could result in large out-of-pocket expenses that might be challenging to cover from regular monthly income sources

- Right-size an emergency fund to each retiree’s needs, and ensure that funds can be accessed quickly

Consider more than just liquidity

Plan for rising health care and long-term care costs

Out-of-pocket health care and long-term care expenses are increasingly the wild cards of retirement income planning. Not only are they among the top spending shocks, but they’re also growing faster than other expenses.

That makes flexibility an even more critical part of each client’s plan. Whether due to federal policy changes, client health events or both, odds are that many retirees will need to grow their savings to cover the ever-increasing cost of health care.

One way to build in this flexibility is by including a mix of income sources: taxable, tax-deferred and tax-free. This gives you more levers to pull when a spending shock happens and allows you to manage the tax impact more efficiently.

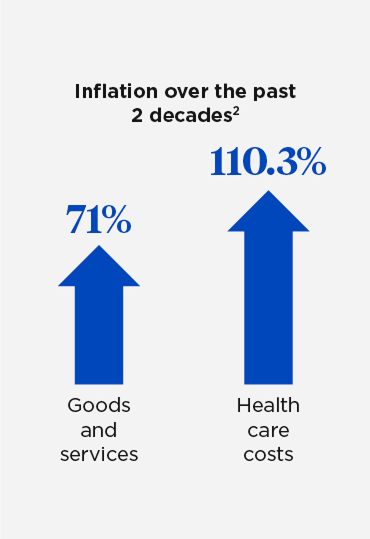

Over the past 20 years, health care costs have risen more than 110%, compared to 71% for all other goods and services.2 As people live longer, the need for long-term care becomes more likely. For instance, many clients don’t realize that Medicare doesn’t cover most long-term care services, which makes planning even more critical.