Loading...

The Effective Marginal Rate: A smart approach to planning tax-efficient retirement withdrawals

By Joe Elsasser, CFP®, President — Covisum

Key takeaways

A client’s tax bracket doesn’t tell the full story in retirement.

The Effective Marginal Rate (EMR) shows the true tax cost of the next dollar withdrawn after accounting for considerations such as Social Security taxation, capital gains taxes, subsidies and Medicare surcharges (IRMAA).

Small withdrawals can trigger unexpectedly high taxes.

Interactions among income sources can and do push tax rates well above a retiree’s stated tax bracket — or create opportunities for you to position low- or no-tax withdrawals.

An approach of planning around the EMR can improve outcomes.

Using the EMR as a guide helps you articulate the importance of tax diversification and withdrawal sequencing strategies to help reduce lifetime taxes.

Most of your retirement-age clients are probably aware of the impact that taxes can have on their retirement savings: The more they save on taxes, the more they can either spend in retirement or pass on to their beneficiaries. Some may even be familiar with marginal tax rates and effective tax rates.

Both marginal and effective tax rates are important concepts. But neither tells the full story in retirement.

Marginal tax rate: Determines the tax owed on the last dollar of income.

Effective tax rate: Found by dividing the total taxes paid by the total taxable income.

What is the Effective Marginal Rate?

To get a fuller view of taxation in retirement, we can turn to the Effective Marginal Rate (EMR). This rate is the net cost on the next dollar of IRA withdrawal or capital gain recognition. This includes the impact of interactions with other types of taxes, such as net investment income tax, or losing tax-return-driven subsidies or surcharges, such as Affordable Care Act premium subsidies or Medicare IRMAA penalties. By understanding and planning around the Effective Marginal Rate, you can help your clients improve retirement income outcomes, lower lifetime tax burdens and keep more of what they’ve saved.

Why retirement taxes are more complicated than they look

During working years, tax planning is often straightforward. Income is primarily wages, and taxes generally rise in a predictable way as earnings increase. In retirement, however, income comes from many different sources — tax-deferred accounts, taxable accounts, Roth assets and Social Security benefits — and each is taxed differently.

That complexity creates interactions that don’t show up when looking only at tax brackets. For example, an additional dollar withdrawn from a tax-deferred account can:

- Cause more Social Security benefits to become taxable

- Push long-term capital gains out of the 0% bracket and into higher rates

- Trigger phaseouts of deductions or credits

- Increase Medicare premiums through income-related monthly adjustment amount (IRMAA) surcharges

- Interact with other provisions such as the net investment income tax (NIIT)

The result is that the tax cost of that "next dollar" withdrawn may be far higher than the retiree expects. In some cases, retirees can face Effective Marginal Rates well above their stated bracket. In others, opportunities exist to withdraw additional funds at very low — or even zero — tax cost.

How to help clients visualize their EMR

The effective marginal rate captures not just ordinary income tax but also the ripple effects that additional income has across the tax return. One way to help clients understand this is through a tax map, which I devised to plot retirement account withdrawals along one axis and the EMR along the other. Instead of a smooth, upward-sloping line, tax maps often reveal spikes and valleys. Spikes represent areas where a small increase in income triggers outsize tax consequences. Valleys represent windows where additional withdrawals can be made at relatively low cost.

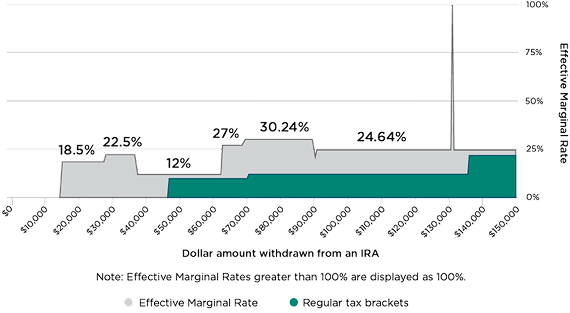

This is an example of a tax map for a hypothetical retired couple over the age of 65.

Let’s assume they have $60,000 of combined Social Security benefits and $30,000 of long-term capital gains. The map starts at $0 of ordinary income on the left and demonstrates the EMR as it moves to the right.

At roughly $15,000 of IRA withdrawals, the couple’s marginal tax rate is 0% since they’re still under their standard deduction. However, they actually see an 18.5% EMR on each dollar withdrawn from the IRA. That’s because each additional dollar withdrawn causes 85 cents of Social Security benefits to become taxable. That same concept pushes the EMR to 22.5% as withdrawals grow.

Once the full taxable portion of Social Security benefits has been reached, the EMR briefly drops back to 12%. It then rises to 27% when additional withdrawals push long-term capital gains out of the 0% bracket and into the 15% bracket.

At higher withdrawal levels, the phaseout of a temporary senior deduction increases the EMR to approximately 30%. It later declines to about 25% once that phaseout is complete.

Next steps: Help clients begin retirement tax planning now

7 in 10 pre-retirees acknowledge they would switch financial professionals for one who could help plan for taxes in retirement.1 Focusing on EMR during tax planning helps you offer clients an elevated level of retirement tax planning — one that delivers a more precise, more practical way to manage the decision of where to pull the next dollar of retirement income. It’s a powerful lens that can reveal new opportunities to improve levels of retirement income or pass on greater levels of wealth to beneficiaries.

To help your clients avoid unintended costs and react to changing tax laws throughout retirement, read my full white paper on tax-efficient retirement income planning.

Download the full white paper

[1] "The Nationwide Retirement Institute 2025 Social Security survey," conducted by The Harris Poll on behalf of the Nationwide Retirement Institute. This online survey was conducted June 2-17, 2025, among 1,812 U.S. adults age 18 or older.