Self-funded solutions

Self-funded solutions

What is stop loss insurance?

Why choose a plan with stop loss coverage?

Protecting a company financially is critical, and stop loss is an employer’s safety net. With the Self-Funded Program through Nationwide, stop loss insurance is included in employers’ monthly payments. This protects the employer against higher-than-expected claims. Combined with level funding, employers can rest assured they’ll never pay more than the agreed-upon amount to fund the claims account each year.

Stop loss coverage in action

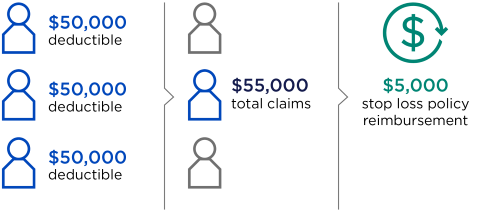

Example A: Plan member-specific deductibles

If an employer chooses a $50,000 specific deductible per plan member for that policy year and a member exceeds that liability with total claims of $55,000, for example, the stop loss coverage will reimburse the employer for the excess $5,000.

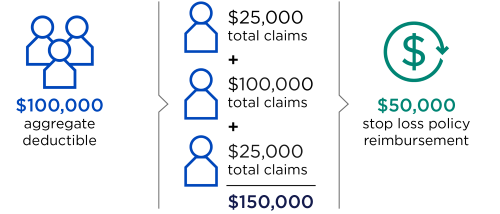

Example B: Aggregate deductible

If an employer’s aggregate deductible is $100,000 for that policy year, and the group exceeds that liability and the total claims are $150,000, the stop loss coverage will reimburse them for the excess amount of $50,000.

Middle market group stop loss

Want to learn more?

Call a sales representative at 1-877-877-0245.