Start by organizing all your debt in one place to get a clear picture of your financial obligations. Whether you prefer a spreadsheet, budgeting app, or notebook, choose a method that works for you.

For each debt, include key details such as:

- Type of debt (e.g., credit card, mortgage, personal loan)

- Monthly payment amount

- Due date

- Interest rate

- Outstanding balance

- Any applicable fees or penalties

Once everything is listed, you’ll have a better understanding of who you owe, how much you owe, and how each debt impacts your finances.

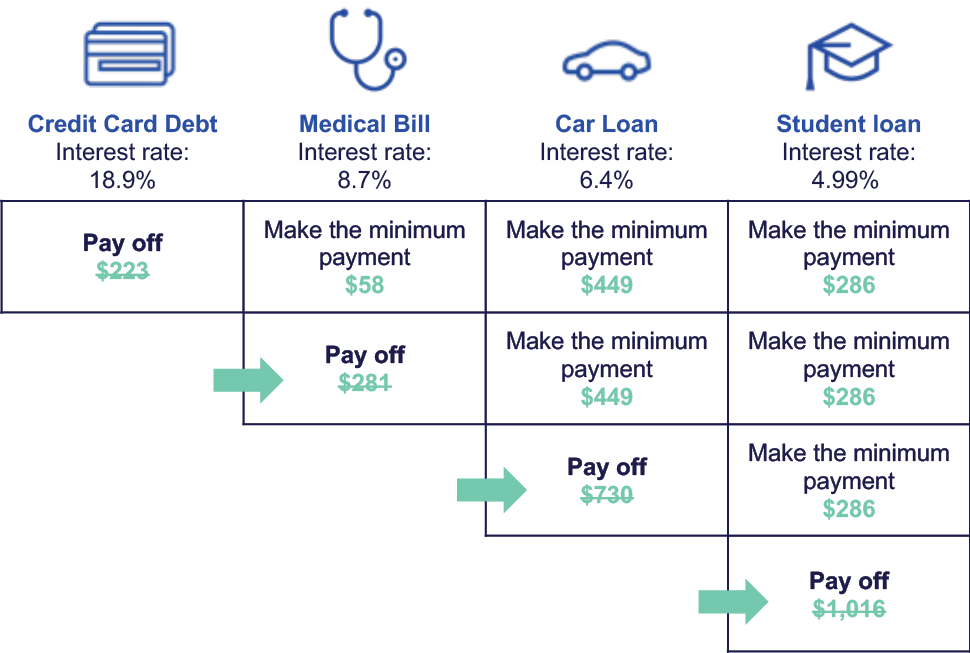

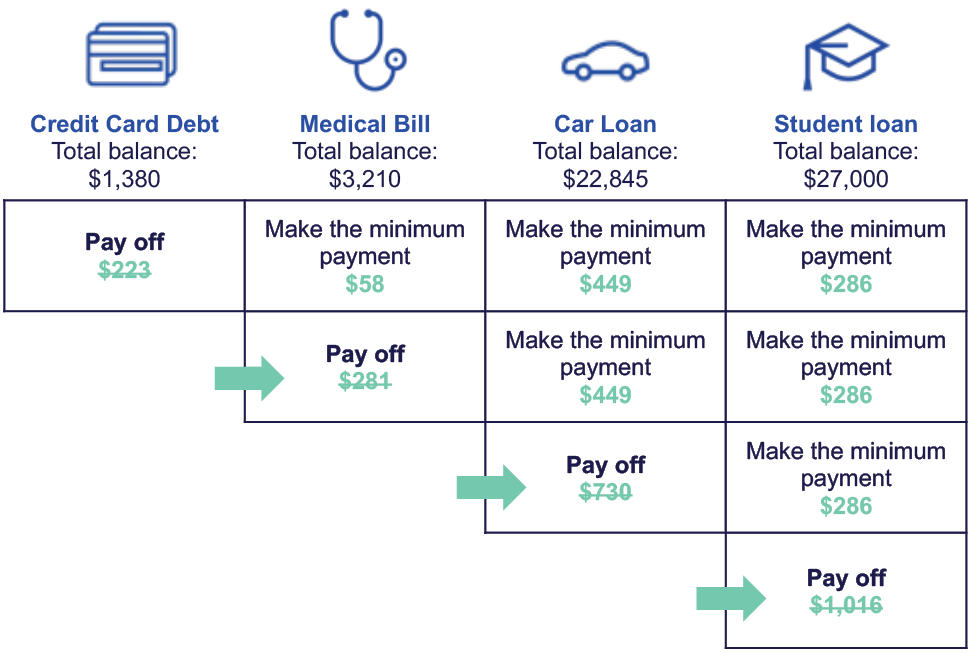

This is also a good time to distinguish between helpful and harmful debt. Debt with lower interest rates and long-term benefits, such as a mortgage, can support your financial goals. In contrast, high-interest debt like credit cards or payday loans can quickly become a burden. Prioritize paying off high-cost debt to reduce financial strain and improve your overall financial health.