1. Build a budget that works for retirement

2. Be strategic about claiming Social Security

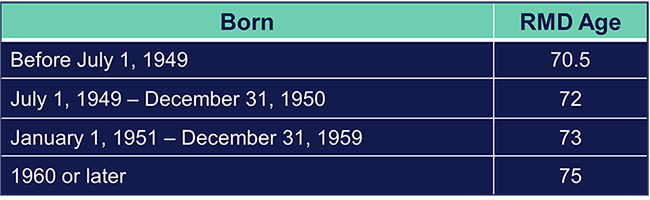

3. Prepare for Required Minimum Distributions (RMDs)

Tax-deferred retirement accounts offer the benefit of postponing taxes, but eventually, the IRS requires you to begin taking withdrawals. These mandatory withdrawals are called required minimum distributions, or RMDs.

RMDs apply to traditional retirement accounts such as 401(k)s. It’s important to take RMDs on time and in the correct amount. Missing a required distribution or withdrawing too little could result in a significant tax penalty, in addition to regular income taxes on the full amount.

If you don’t need the income when RMDs begin, consider working with a financial professional. They can help you explore strategies to manage your distributions in a way that aligns with your goals and may reduce your tax burden.

Once you reach the age when required minimum distributions begin, you’ll need to take your first withdrawal by April 1 of the year following the year you reach that age. After that, RMDs must be taken by December 31 each year.

If you delay your first withdrawal until the following year, you’ll need to take two RMDs in that year. This could increase your taxable income and potentially place you in a higher tax bracket.

If you’re still working and contributing to your employer’s retirement plan when you reach your RMD age, you may be able to delay RMDs from that specific account until after you leave the company.

To calculate your RMD, divide your account balance as of December 31 of the previous year by a life expectancy factor based on your age. These factors are published in IRS Publication 590-B (PDF). If your retirement account is with a provider that offers RMD services, they may automatically calculate and distribute the correct amount for you each year.

4. Know how taxes affect retirement income

How Retirement Income Is Taxed

Understanding how different types of retirement income are taxed can help you plan more effectively and avoid surprises at tax time. Here’s a breakdown of how various income sources may be treated:

5. Take Control of Debt in Retirement

For more insights on living in retirement, review our resources for soon-to-be and current retirees.