Investing & retirement resources

Investing & retirement resources

Retirement advice from real retirees

10 retirement planning tips to consider

Who better to ask how to plan for retirement than those who are living it now? Nationwide and consumer research company Yankelovich surveyed current retirees to find out their firsthand retirement advice.

1. Monitor your investments in pre-retirement

Money needed 5-10 years into retirement is most vulnerable, so avoid overspending. If that money is lost, it is harder to recover over time. Look for investments with predictable income sources, but remember the more predictable the income, the lower the return.

2. Plan for inflation as a fact of life

Inflation and rising prices can eat away at the buying power of retirement funds. When planning for retirement, just assume prices will go up – and be planning for it.

3. Talk with your spouse or significant other about retirement spending

Be open with your spouse or significant other about how much you think you should, and will, spend in retirement so that you’re both on the same page. Just as couples discuss buying a new car or a house while working, it’s always a good habit to talk though financial matters in retirement as well.

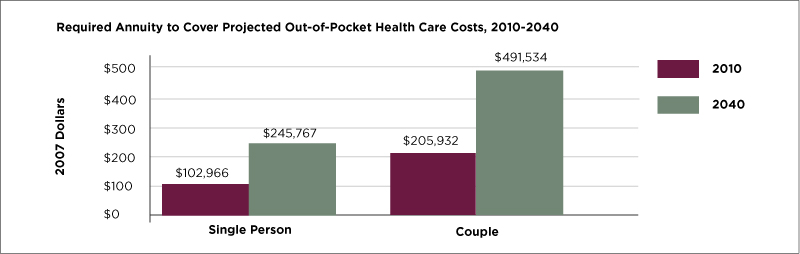

4. Focus on physical health

Given the high costs of health care, focusing on physical fitness today is key to staying fiscally fit in retirement. Health care costs are often overlooked by retirees, despite the fact that it’s constantly in the news and is still spinning out of control. Health care expenses could really burden your finances when you consider the projections:

5. Create a budget and follow it

The best way to plan a budget is to know how much you can spend. But alas, most people don’t bother to calculate how much they can safely spend in retirement. If you need help starting out, meet with an investment professional, like the majority of people who said they calculated their annual spending in retirement. An investment professional can provide additional insight and tools to help you stay on track with your plan. Speaking of which…

6. Get a good investment professional

You go to the doctor to help you stay healthy, so having an investment professional you work with regularly is a smart way to plan for fiscal health in retirement. Ask friends for recommendations on who they use, since referrals are often the best way to locate a good investment professional.

7. Watch travel expenses in retirement

Travel is cheaper and easier when you’re mobile, so take big trips when you are younger. Don’t save all of your vacations for retirement as this will be more costly. Also, don’t take overly expensive vacations. As you are smart about spending when at home, keep the same habits while traveling.

8. Pay off your mortgage

Your home is more than just shelter, it also comprises a significant contribution to your fixed expenses. By paying off your mortgage you can finally tap into your home’s wealth by living there “rent-free” – eliminating a significant monthly expense.

9. Work longer

One of the best ways to ensure you have sufficient money well into retirement is to work a few additional years, beyond what you originally had planned. It may not be what you want to do, but it will add more cushion to your nest egg in the long run. Even just a couple more years of work income can add significantly to your retirement funds.

10. Expect to spend more

No matter how much you plan, surprise expenses are inevitable. Budget for unexpected expenses, as well as costs like property taxes and household maintenance costs that may go up dramatically during retirement.

The overall good news is that making a few small changes – maybe working a few years longer, saving a bit more each month and adopting some healthy lifestyle habits – can add up to a much more comfortable retirement. Talk to an investment professional about how you can save for retirement and be prepared.

Want to work with a financial professional?

Call 1-877-245-0761