What you'll learn:

What is a credit score?

Why does a credit score matter?

Want ideas to improve your credit score?

What goes into your credit score?

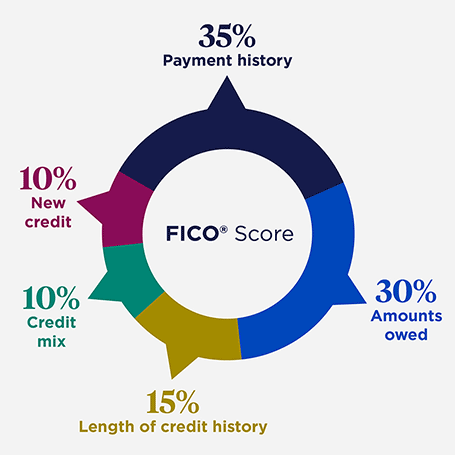

FICO and VantageScore weigh these factors differently, but both look at the same general categories. Here are 5 of the main factors that can shape your score.

1. Payment history

This is the biggest factor. It reflects whether you pay your bills on time. A payment typically isn’t reported late until it’s at least 30 days past due, but once it is, the impact can be significant.

2. Amounts owed (credit utilization)

This looks at how much of your available credit you’re using. Using a high percentage of your credit can signal higher risk to lenders. Keeping utilization under 30% — and ideally under 10% — supports a healthier score.

3. Length of credit history

This includes how long your accounts have been open and how long it’s been since you used them. A longer history generally helps your score.

4. Credit mix

Lenders like to see that you can handle different types of credit, such as credit cards, student loans, auto loans or a mortgage.

5. New credit

Opening several new accounts in a short period can lower your score temporarily. Hard inquiries — the checks lenders run when you apply for credit — show up here.

VantageScore differences

VantageScore models weigh these factors slightly differently. For example, payment history makes up about 40% of a VantageScore 3.0 score, compared with 35% in the FICO model. The categories, however, remain similar across both.

Where credit score information comes from

Your score is built from the data in your credit reports, which are maintained by 3 nationwide credit reporting agencies: Equifax, Experian and TransUnion. They collect information from lenders about your balances, payment history and account status.

How to check your credit reports and scores

You can get free copies of your credit reports from all 3 credit bureaus once a year at annualcreditreport.com. These reports include the information used to calculate your score but not the score itself.

Your credit score may be available through your bank, credit card company or certain financial apps, depending on the institution.

Ready to put these ideas into action?

Use our article, "30-day plan to build your credit score," as a 4-week checklist.